Page 18 - Chap7 ITC

P. 18

Answer : Computation of ITC available with V-Supply Pvt. Ltd. for the tax period:

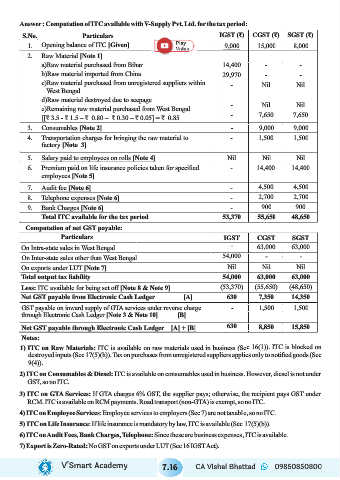

S.No. Particulars IGST (₹) CGST (₹) SGST (₹)

1. Opening balance of ITC [Given] 9,000 15,000 8,000

2. Raw Material [Note 1]

a) Raw material purchased from Bihar 14,400 - -

b) Raw material imported from China 29,970 - -

c) Raw material purchased from unregistered suppliers within

- Nil Nil

West Bengal

d) Raw material destroyed due to seepage

- Nil Nil

e) Remaining raw material purchased from West Bengal

- 7,650 7,650

[[₹ 3.5 - ₹ 1.5 – ₹ 0.80 – ₹ 0.30 – ₹ 0.05] = ₹ 0.85

3. Consumables [Note 2] - 9,000 9,000

4. Transportation charges for bringing the raw material to - 1,500 1,500

factory [Note 3]

5. Salary paid to employees on rolls [Note 4] Nil Nil Nil

6. Premium paid on life insurance policies taken for specified - 14,400 14,400

employees [Note 5]

7. Audit fee [Note 6] - 4,500 4,500

8. Telephone expenses [Note 6] - 2,700 2,700

9. Bank Charges [Note 6] - 900 900

Total ITC available for the tax period 53,370 55,650 48,650

Computation of net GST payable:

Particulars IGST CGST SGST

On Intra-state sales in West Bengal - 63,000 63,000

On Inter-state sales other than West Bengal 54,000 - -

On exports under LUT [Note 7] Nil Nil Nil

Total output tax liability 54,000 63,000 63,000

Less: ITC available for being set off [Note 8 & Note 9] (53,370) (55,650) (48,650)

Net GST payable from Electronic Cash Ledger [A] 630 7,350 14,350

GST payable on inward supply of GTA services under reverse charge - 1,500 1,500

through Electronic Cash Ledger [Note 3 & Note 10] [B]

Net GST payable through Electronic Cash Ledger [A] + [B] 630 8,850 15,850

Notes:

1) ITC on Raw Materials: ITC is available on raw materials used in business (Sec 16(1)). ITC is blocked on

destroyed inputs (Sec 17(5)(h)). Tax on purchases from unregistered suppliers applies only to notified goods (Sec

9(4)).

2) ITC on Consumables & Diesel: ITC is available on consumables used in business. However, diesel is not under

GST, so no ITC.

3) ITC on GTA Services: If GTA charges 6% GST, the supplier pays; otherwise, the recipient pays GST under

RCM. ITC is available on RCM payments. Road transport (non-GTA) is exempt, so no ITC.

4) ITC on Employee Services: Employee services to employers (Sec 7) are not taxable, so no ITC.

5) ITC on Life Insurance: If life insurance is mandatory by law, ITC is available (Sec 17(5)(b)).

6) ITC on Audit Fees, Bank Charges, Telephone: Since these are business expenses, ITC is available.

7) Export is Zero-Rated: No GST on exports under LUT (Sec 16 IGST Act).

V’Smart Academy 7.16 CA Vishal Bhattad 09850850800