Page 12 - Ch15_Computation of GST

P. 12

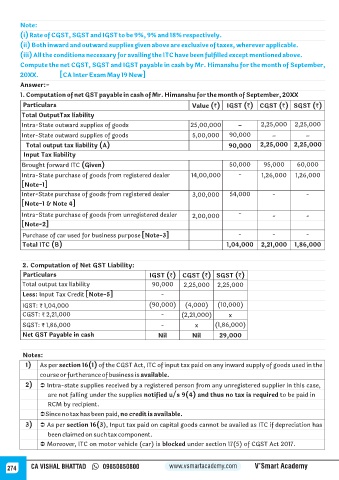

Note:

(i) Rate of CGST, SGST and IGST to be 9%, 9% and 18% respectively.

(ii) Both inward and outward supplies given above are exclusive of taxes, wherever applicable.

(iii) All the conditions necessary for availing the ITC have been fulfilled except mentioned above.

Compute the net CGST, SGST and IGST payable in cash by Mr. Himanshu for the month of September,

20XX. [CA Inter Exam May 19 New]

Answer:-

1. Computation of net GST payable in cash of Mr. Himanshu for the month of September, 20XX

Particulars Value (`) IGST (`) CGST (`) SGST (`)

Total OutputTax liability

Intra-State outward supplies of goods 25,00,000 _ 2,25,000 2,25,000

Inter-State outward supplies of goods 5,00,000 90,000 _ _

Total output tax liability (A) 90,000 2,25,000 2,25,000

Input Tax liability

Brought forward ITC (Given) 50,000 95,000 60,000

Intra-State purchase of goods from registered dealer 14,00,000 - 1,26,000 1,26,000

[Note-1]

Inter-State purchase of goods from registered dealer 3,00,000 54,000 - -

[Note-1 & Note 4]

Intra-State purchase of goods from unregistered dealer 2,00,000 - - -

[Note-2]

Purchase of car used for business purpose [Note-3] - - -

Total ITC (B) 1,04,000 2,21,000 1,86,000

2. Computation of Net GST Liability:

Particulars IGST (`) CGST (`) SGST (`)

Total output tax liability 90,000 2,25,000 2,25,000

Less: Input Tax Credit [Note-5] -

IGST: ₹ 1,04,000 (90,000) (4,000) (10,000)

CGST: ₹ 2,21,000 - (2,21,000) x

SGST: ₹ 1,86,000 - x (1,86,000)

Net GST Payable in cash Nil Nil 29,000

Notes:

1) As per section 16(1) of the CGST Act, ITC of input tax paid on any inward supply of goods used in the

course or furtherance of business is available.

2) Ü Intra-state supplies received by a registered person from any unregistered supplier in this case,

are not falling under the supplies notified u/s 9(4) and thus no tax is required to be paid in

RCM by recipient.

ÜSince no tax has been paid, no credit is available.

3) Ü As per section 16(3), Input tax paid on capital goods cannot be availed as ITC if depreciation has

been claimed on such tax component.

Ü Moreover, ITC on motor vehicle (car) is blocked under section 17(5) of CGST Act 2017.

274 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy