Page 5 - Ch8_ EXEMPTION

P. 5

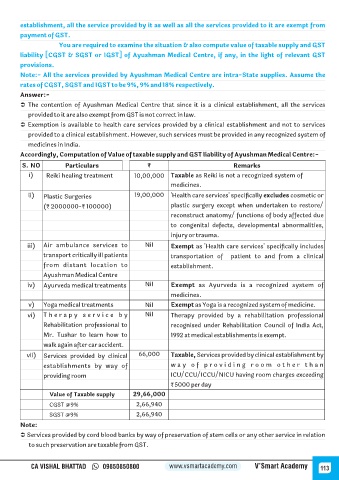

establishment, all the service provided by it as well as all the services provided to it are exempt from

payment of GST.

You are required to examine the situation & also compute value of taxable supply and GST

liability [CGST & SGST or IGST] of Ayushman Medical Centre, if any, in the light of relevant GST

provisions.

Note:- All the services provided by Ayushman Medical Centre are intra-State supplies. Assume the

rates of CGST, SGST and IGST to be 9%, 9% and 18% respectively.

Answer:-

Ü The contention of Ayushman Medical Centre that since it is a clinical establishment, all the services

provided to it are also exempt from GST is not correct in law.

Ü Exemption is available to health care services provided by a clinical establishment and not to services

provided to a clinical establishment. However, such services must be provided in any recognized system of

medicines in India.

Accordingly, Computation of Value of taxable supply and GST liability of Ayushman Medical Centre:-

S. NO Particulars ₹ Remarks

i) Reiki healing treatment 10,00,000 Taxable as Reiki is not a recognized system of

medicines.

ii) Plastic Surgeries 19,00,000 'Health care services' specifically excludes cosmetic or

(₹ 2000000-₹ 100000) plastic surgery except when undertaken to restore/

reconstruct anatomy/ functions of body affected due

to congenital defects, developmental abnormalities,

injury or trauma.

iii) Air ambulance services to Nil Exempt as 'Health care services' specifically includes

transport critically ill patients transportation of patient to and from a clinical

from distant location to establishment.

Ayushman Medical Centre

iv) Ayurveda medical treatments Nil Exempt as Ayurveda is a recognized system of

medicines.

v) Yoga medical treatments Nil Exempt as Yoga is a recognized system of medicine.

vi) T h e r a p y s e r v i c e b y Nil Therapy provided by a rehabilitation professional

Rehabilitation professional to recognised under Rehabilitation Council of India Act,

Mr. Tushar to learn how to 1992 at medical establishments is exempt.

walk again after car accident.

vii) Services provided by clinical 66,000 Taxable, Services provided by clinical establishment by

establishments by way of w a y o f p r o v i d i n g r o o m o t h e r t h a n

providing room ICU/CCU/ICCU/NICU having room charges exceeding

₹ 5000 per day

Value of Taxable supply 29,66,000

CGST @9% 2,66,940

SGST @9% 2,66,940

Note:

Ü Services provided by cord blood banks by way of preservation of stem cells or any other service in relation

to such preservation are taxable from GST.

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 113