Page 290 - CA Inter Audit PARAM

P. 290

CA Ravi Taori

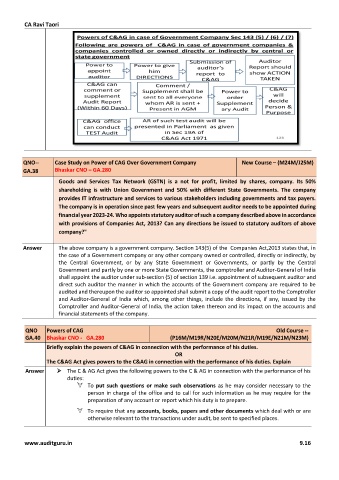

QNO-- Case Study on Power of CAG Over Government Company New Course – (M24M/J25M)

GA.38 Bhaskar CNO – GA.280

Goods and Services Tax Network (GSTN) is a not for profit, limited by shares, company. Its 50%

shareholding is with Union Government and 50% with different State Governments. The company

provides IT infrastructure and services to various stakeholders including governments and tax payers.

The company is in operation since past few years and subsequent auditor needs to be appointed during

financial year 2023-24. Who appoints statutory auditor of such a company described above in accordance

with provisions of Companies Act, 2013? Can any directions be issued to statutory auditors of above

company?"

Answer The above company is a government company. Section 143(5) of the Companies Act,2013 states that, in

the case of a Government company or any other company owned or controlled, directly or indirectly, by

the Central Government, or by any State Government or Governments, or partly by the Central

Government and partly by one or more State Governments, the comptroller and Auditor-General of India

shall appoint the auditor under sub-section (5) of section 139 i.e. appointment of subsequent auditor and

direct such auditor the manner in which the accounts of the Government company are required to be

audited and thereupon the auditor so appointed shall submit a copy of the audit report to the Comptroller

and Auditor-General of India which, among other things, include the directions, if any, issued by the

Comptroller and Auditor-General of India, the action taken thereon and its impact on the accounts and

financial statements of the company.

QNO Powers of CAG Old Course --

GA.40 Bhaskar CNO - GA.280 (P16M/M19R/N20E/M20M/N21R/M19E/N21M/N23M)

Briefly explain the powers of C&AG in connection with the performance of his duties.

OR

The C&AG Act gives powers to the C&AG in connection with the performance of his duties. Explain

Answer ➢ The C & AG Act gives the following powers to the C & AG in connection with the performance of his

duties:

To put such questions or make such observations as he may consider necessary to the

person in charge of the office and to call for such information as he may require for the

preparation of any account or report which his duty is to prepare.

To require that any accounts, books, papers and other documents which deal with or are

otherwise relevant to the transactions under audit, be sent to specified places.

www.auditguru.in 9.16