Page 69 - CA Inter Bhaskar Vol 1

P. 69

CA RAVI TAORI AUDIT RISK & ITs’ COMPONENTS (QNO-315.01, 315.01.20, 315.01.50, 315.01.60, 315.01.70, 315.01.80,

RISK ASSESSMENT AND INTERNAL CONTROL

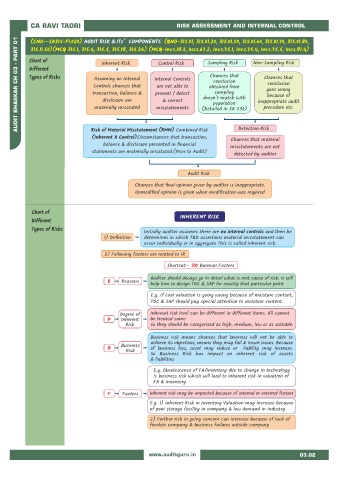

AUDIT BHASKAR CH 03 - PART 01 Chart of transaction, balance & Internal Controls (Detailed in SA 530) Non-Sampling Risk

(CNO SA315-P1.020) --

75 1, I.

75 5, Incs.81.4).

75.4, Incs.

ncs.

315.11.50)(MCQ 315.1, 315.4, 315.5, 315.18, 315.26) (MCQ-Incs.18.3, Incs.67.2, Incs.

Sampling Risk

Inherent Risk

Control Risk

Different

Chances that

Types of Risks

Chances that

Assuming no Internal

conclusion

conclusion

Controls chances that

are not able to

obtained from

goes wrong

sampling

prevent / detect

because of

doesn't match with

disclosure are

& correct

inappropriate audit

population

materially misstated

procedure etc.

misstatements

Risk of Material Misstatement (RMM) Combined Risk

(Inherent X Control)Circumstances that transaction, Detection Risk

Chances that material

balance & disclosure presented in financial

misstatements are not

statements are materially misstated.(Prior to Audit)

detected by auditor

Audit Risk

Chances that final opinion given by auditor is inappropriate.

Unmodified opinion is given when modification was required

Chart of

INHERENT RISK

Different

Types of Risks

Initially auditor assumes there are no internal controls and then he

1) Definition determines in which TBD assertions material misstatement can

occur Individually or in aggregate This is called inherent risk.

2) Following factors are related to IR

Shortcut:- RD Burman Factors

Auditor should always go in detail what is root cause of risk. It will

R Reasons

help him to design TOC & SAP for exactly that particular point

E.g. If coal valuation is going wrong because of moisture content,

TOC & SAP should pay special attention to moisture content.

Degree of Inherent risk level can be different in different items. All cannot

D Inherent be treated same

Risk So they should be categorised as high, medium, low or as suitable.

Business risk means chances that business will not be able to

achieve its objectives, means they may fail & incurr losses. Because

Business

B of business loss, asset may reduce or liability may increase.

Risk

So Business Risk has impact on inherent risk of assets

& liabilities

E.g. Obsolescence of FA/Inventory due to change in technology

is business risk which will lead to inherent risk in valuation of

FA & Inventory

F Factors Inherent risk may be impacted because of internal or external factors

E.g. 1) Inherent Risk in Inventory Valuation may increase because

of poor storage facility in company & low demand in industry

2) Further risk in going concern can increase because of lack of

fundsin company & business failures outside company

www.auditguru.in 03.02