Page 72 - CA Inter Bhaskar Vol 1

P. 72

RISK ASSESSMENT AND INTERNAL CONTROL CA RAVI TAORI

Accordingly, some control risk will always exist. The SAs provide the conditions under which the

auditor is required to, or may choose to, test the operating effectiveness of controls in determining

the nature, timing and extent of substantive procedures to be performed.

Combined Vs Separate Assessment

The SAs do not ordinarily refer to inherent risk and control risk separately, but rather to a combined AUDIT BHASKAR CH 03 - PART 01

assessment of the “risks of material misstatement”. However, the auditor may make separate or

combined assessments of inherent and control risk depending on preferred audit techniques or

methodologies and practical considerations. The assessment of the risks of material

misstatement may be expressed in quantitative terms, such as in percentages, or in non-

quantitative terms. In any case, the need for the auditor to make appropriate risk assessments is

more important than the different approaches by which they may be made.

(In big assignments go for separate analysis, further if auditor is relying extensively on test of

controls, then separate analysis id preferred)

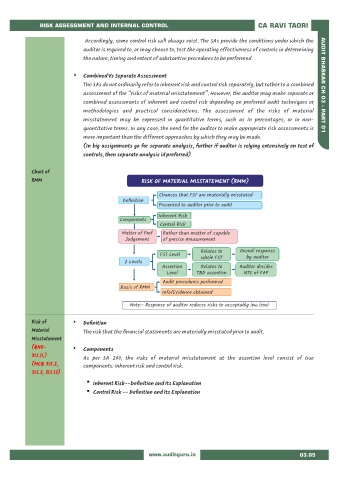

Chart of

RMM RISK OF MATERIAL MISSTATEMENT (RMM)

Chances that FST are materially misstated

Definition

Presented to auditor prior to audit

Inherent Risk

Components

Control Risk

Matter of Prof Rather than matter of capable

Judgement of precise measurement

Relates to Overall response

FST Level

whole FST by auditor

2 Levels

Assertion Relates to Auditor decides

Level TBD assertion NTE of FAP

Audit procedures performed

Basis of RMM

Info/Evidence obtained

Note:- Response of auditor reduces risks to acceptably low level

Risk of Definition

Material The risk that the financial statements are materially misstated prior to audit.

Misstatement

(QNO- Components

315.11.)

As per SA 200, the risks of material misstatement at the assertion level consist of two

(MCQ 315.2, components: inherent risk and control risk.

315.3, 315.13)

Inherent Risk--Definition and Its Explanation

Control Risk -- Definition and Its Explanation

www.auditguru.in 03.05