Page 74 - CA Inter Bhaskar Vol 1

P. 74

RISK ASSESSMENT AND INTERNAL CONTROL CA RAVI TAORI

Detection Risk Meaning: -

(MCQ-315.10) The risk that the procedures performed by the auditor to reduce audit risk to an acceptably low

level will not detect a misstatement that exists and that could be material, either individually or

when aggregated with other misstatements.

Suppose auditor of a company uses certain audit procedures for the purpose of obtaining audit

evidence and reducing audit risk, but still there will remain a risk that audit procedures used by the

auditor may not be able to detect a misstatement which by nature is material, then that risk is AUDIT BHASKAR CH 03 - PART 01

known as Detection Risk.

Example

While auditing the books of accounts of Grateful Limited for the financial year 2020-21, the

auditor of the above mentioned company used various audit procedures, for example-observation,

inspection, reperformance, recalculation etc for obtaining audit evidence regarding stock, Debtors,

sales, purchases etc., and consequently reducing the audit risk. However, there will always remain

a risk that various audit procedures as used by auditor of Grateful Limited will not be able to detect

misstatements which are material in nature. This risk is known as Detection Risk.

Interrelationship of the components of audit risk:

Inherent and control risks differ from detection risk in that they exist independently of an audit of

financial information. Inherent and control risks are functions of the entity's business and its

environment and the nature of the account balances or classes of transactions, regardless of

whether an audit is conducted.

Even though inherent and control risks cannot be controlled by the auditor, the auditor can assess

them and design his substantive procedures to produce an acceptable level of detection risk,

thereby reducing audit risk to an acceptably low level.

For a given level of audit risk, the acceptable level of detection risk bears an inverse relationship to

the assessed risks of material misstatement at the assertion level. For example, the greater the

risks of material misstatement the auditor believes exists, the less the detection risk that can be

accepted and, accordingly, the more persuasive the audit evidence required by the auditor.

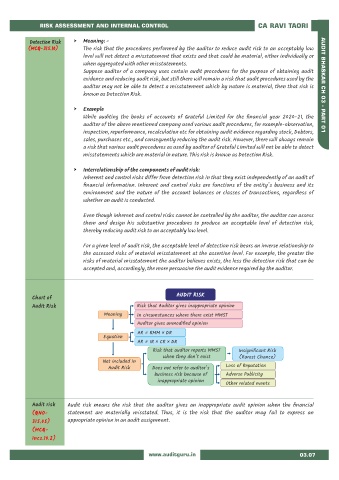

AUDIT RISK

Chart of

Audit Risk Risk that Auditor gives inappropriate opinion

Meaning In circumstances where there exist MMST

Auditor gives unmodified opinion

AR = RMM × DR

Equation

AR = IR × CR × DR

Risk that auditor reports MMST Insignificant Risk

when they don't exist (Rarest Chance)

Not included in

Loss of Reputation

Audit Risk Does not refer to auditor's

business risk because of Adverse Publicity

inappropriate opinion

Other related events

Audit risk Audit risk means the risk that the auditor gives an inappropriate audit opinion when the financial

(QNO- statement are materially misstated. Thus, it is the risk that the auditor may fail to express an

315.05) appropriate opinion in an audit assignment.

(MCQ-

Incs.10.2)

www.auditguru.in 03.07