Page 71 - CA Inter Bhaskar Vol 1

P. 71

CA RAVI TAORI CONTROL RISK (CR)

RISK ASSESSMENT AND INTERNAL CONTROL

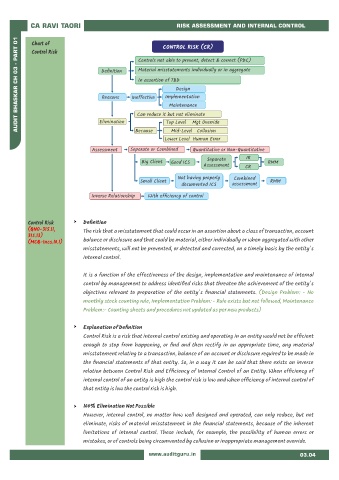

AUDIT BHASKAR CH 03 - PART 01 Definition Ineffective Implementation

Chart of

Control Risk

Controls not able to prevent, detect & correct (PDC)

Material misstatements individually or in aggregate

In assertion of TBD

Design

Reasons

Maintenance

Can reduce it but not eliminate

Elimination

Top Level Mgt Override

Because

Mid-Level Collusion

Lower Level Human Error

Assessment Separate or Combined Quantitative or Non-Quantitative

Separate IR

Big Client Good ICS RMM

Assessment CR

Not having properly Combined

Small Client RMM

documented ICS assessment

Inverse Relationship With efficiency of control

Control Risk Definition

(QNO-315.11, The risk that a misstatement that could occur in an assertion about a class of transaction, account

315.13)

(MCQ-Incs.10.1) balance or disclosure and that could be material, either individually or when aggregated with other

misstatements, will not be prevented, or detected and corrected, on a timely basis by the entity's

internal control.

It is a function of the effectiveness of the design, implementation and maintenance of internal

control by management to address identified risks that threaten the achievement of the entity's

objectives relevant to preparation of the entity's financial statements. (Design Problem: - No

monthly stock counting rule, Implementation Problem: - Rule exists but not followed, Maintenance

Problem:- Counting sheets and procedures not updated as per new products)

Explanation of Definition

Control Risk is a risk that internal control existing and operating in an entity would not be efficient

enough to stop from happening, or find and then rectify in an appropriate time, any material

misstatement relating to a transaction, balance of an account or disclosure required to be made in

the financial statements of that entity. So, in a way it can be said that there exists an inverse

relation between Control Risk and Efficiency of Internal Control of an Entity. When efficiency of

internal control of an entity is high the control risk is low and when efficiency of internal control of

that entity is low the control risk is high.

100% Elimination Not Possible

However, internal control, no matter how well designed and operated, can only reduce, but not

eliminate, risks of material misstatement in the financial statements, because of the inherent

limitations of internal control. These include, for example, the possibility of human errors or

mistakes, or of controls being circumvented by collusion or inappropriate management override.

www.auditguru.in 03.04