Page 82 - CA Inter Bhaskar Vol 1

P. 82

RISK ASSESSMENT AND INTERNAL CONTROL CA RAVI TAORI

2. Regulatory Environment

Understand the applicable financial reporting framework and industry-specific accounting

practices.

Review laws and regulations significantly affecting the entity’s operations, including taxation

and direct regulatory supervision.

Consider the impact of government policies and environmental regulations relevant to the AUDIT BHASKAR CH 03 - PART 01

entity’s business and industry.

3. Other External Factors

Analyse economic conditions, such as GDP trends, inflation, and market volatility.

Assess interest rates and availability of financing, which may influence the entity’s financial

risk and decision-making.

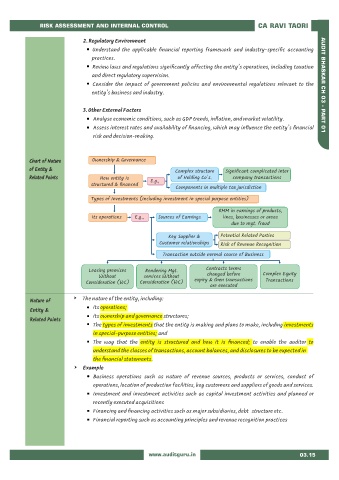

Chart of Nature Ownership & Governance

of Entity & Complex structure Significant complicated inter

Related Points How entity is E.g., of Holding Co's. company transactions

structured & financed

Components in multiple tax jurisdiction

Types of Investments (Including investment in special purpose entities)

RMM in earnings of products,

Its operations E.g., Sources of Earnings lines, businesses or areas

due to mgt. fraud

Key Supplier & Potential Related Parties

Customer relationships Risk of Revenue Recognition

Transaction outside normal course of Business

Contracts terms

Leasing premises Rendering Mgt.

Without services Without changed before Complex Equity

Consideration (WC) Consideration (WC) expiry & then transactions Transactions

are executed

Nature of The nature of the entity, including:

its operations;

Entity &

its ownership and governance structures;

Related Points

The types of investments that the entity is making and plans to make, including investments

in special-purpose entities; and

The way that the entity is structured and how it is financed; to enable the auditor to

understand the classes of transactions, account balances, and disclosures to be expected in

the financial statements.

Example

Business operations such as nature of revenue sources, products or services, conduct of

operations, location of production facilities, key customers and suppliers of goods and services.

Investment and investment activities such as capital investment activities and planned or

recently executed acquisitions

Financing and financing activities such as major subsidiaries, debt structure etc.

Financial reporting such as accounting principles and revenue recognition practices

www.auditguru.in 03.15