Page 81 - CA Inter Bhaskar Vol 1

P. 81

CA RAVI TAORI The auditor shall obtain an understanding of the following:

RISK ASSESSMENT AND INTERNAL CONTROL

AUDIT BHASKAR CH 03 - PART 01 (a) Relevant industry, regulatory, and other external factors including the applicable financial

Obtain

Understanding

reporting framework.

(b) The nature of the entity, including:

(i) its operations;

(ii) its ownership and governance structures;

(iii) the types of investments that the entity is making and plans to make, including

investments in special-purpose entities; and

(iv) the way that the entity is structured and how it is financed;

to enable the auditor to understand the classes of transactions, account balances, and

disclosures to be expected in the financial statements.

(c) The entity's selection and application of accounting policies, including the reasons for

changes thereto. The auditor shall evaluate whether the entity's accounting policies are

appropriate for its business and consistent with the applicable financial reporting framework

and accounting policies used in the relevant industry.

(d) The entity's objectives and strategies, and those related business risks that may result in risks

of material misstatement.

(e) The measurement and review of the entity's financial performance.

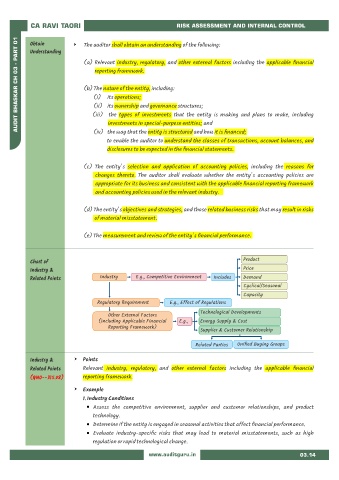

Chart of Product

Industry & Price

Related Points Industry E.g., Competitive Environment Includes Demand

Cyclical/Seasonal

Capacity

Regulatory Requirement E.g., Effect of Regulations

Technological Developments

Other External Factors

(Including Applicable Financial E.g., Energy Supply & Cost

Reporting Framework)

Supplier & Customer Relationship

Related Parties Unified Buying Groups

Industry & Points

Related Points Relevant industry, regulatory, and other external factors including the applicable financial

(QNO--315.08) reporting framework.

Example

1. Industry Conditions

Assess the competitive environment, supplier and customer relationships, and product

technology.

Determine if the entity is engaged in seasonal activities that affect financial performance.

Evaluate industry-specific risks that may lead to material misstatements, such as high

regulation or rapid technological change.

www.auditguru.in 03.14