Page 20 - Chapter 10 Registration

P. 20

State taxable supplies of goods is as under:- In the given case, Mahadev Enterprises is engaged in exclusive intra-State supply of

(I)` 10 lakh for the States of Mizoram, Tripura, Manipur and Nagaland. goods from Himachal Pradesh, Tripura and Uttarakhand.

(ii)` 20 lakh for the States of Arunachal Pradesh, Meghalaya, Puducherry, Sikkim, However, since Mahadev Enterprises makes taxable supply of goods from one

Telangana and Uttarakhand. of the specified Special Category States (i.e. Tripura), it will not be eligible for the

(iii) ` 40 lakh for rest of India. higher threshold limit of ` 40 lakh; instead, the threshold limit for registration will be

The threshold limit for a person making exclusive taxable supply of services or supply reduced to ` 10 lakh

of both goods and services is as under:- (1) In view of the above-mentioned provisions, Mahadev Enterprises is liable to be

(i) ` 10 lakh for the States of Mizoram, Tripura, Manipur and Nagaland. registered under GST law with the aggregate turnover amounting to ` 56,90,000

(ii) ` 20 lakh for the rest of India. (computed on all India basis). The applicable threshold limit of registration in

As per section 2(6), aggregate turnover includes the aggregate value of: this case is ` 10 lakh.

(i) all taxable supplies, Further, he is not liable to be registered in Uttarakhand since he is

CH 10 (ii) all exempt supplies, not making any taxable supply from Uttarakhand.

(iii) exports of goods and/or services and (2) (a) If Mahadev Enterprises is dealing in supply of goods only from Himachal

Registration The above is computed on all India basis. Pradesh, the applicable threshold limit of registration would be ` 40 lakh.

(iv) all inter-State supplies of persons having the same PAN.

In the light of the afore-mentioned provisions, the aggregate turnover of Mahadev

Thus, Mahadev Enterprises will not be liable for registration as its aggregate

turnover would be ` 22,50,000.

Enterprises is computed as under:

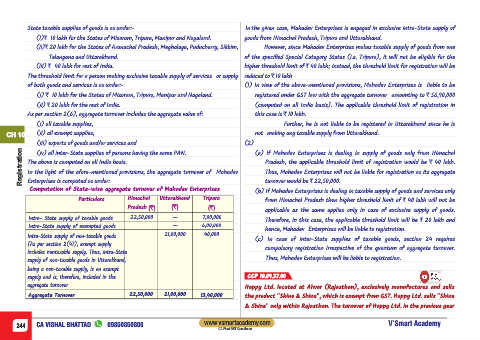

Computation of State-wise aggregate turnover of Mahadev Enterprises (b) If Mahadev Enterprises is dealing in taxable supply of goods and services only

Particulars Himachal Uttarakhand Tripura from Himachal Pradesh then higher threshold limit of ` 40 lakh will not be

Pradesh (`) (`) (`) applicable as the same applies only in case of exclusive supply of goods.

Intra- State supply of taxable goods 22,50,000 - 7,00,000 Therefore, in this case, the applicable threshold limit will be ` 20 lakh and

Intra-State supply of exempted goods - 6,00,000

hence, Mahadev Enterprises will be liable to registration.

Intra-State supply of non-taxable goods 21,00,000 40,000

(c) In case of inter-State supplies of taxable goods, section 24 requires

[As per section 2(47), exempt supply

compulsory registration irrespective of the quantum of aggregate turnover.

includes nontaxable supply. Thus, intra-State

Thus, Mahadev Enterprises will be liable to registration.

supply of non-taxable goods in Uttarakhand,

being a non-taxable supply, is an exempt

supply and is, therefore, included in the CCP 10.09.37.00

aggregate turnover Happy Ltd. located at Alwar (Rajasthan), exclusively manufactures and sells

Aggregate Turnover 22,50,000 21,00,000 13,40,000 the product "Shine & Shine", which is exempt from GST. Happy Ltd. sells "Shine

& Shine" only within Rajasthan. The turnover of Happy Ltd. in the previous year

www.vsmartacademy.com

244 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner