Page 19 - Chapter 10 Registration

P. 19

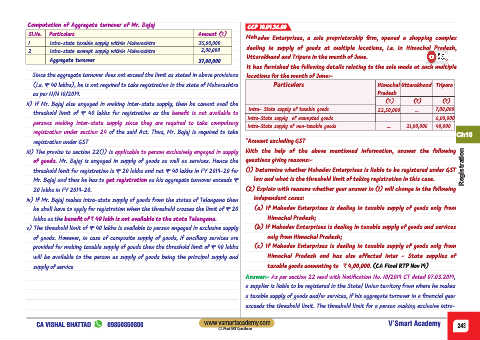

Computation of Aggregate turnover of Mr. Bajaj CCP 10.09.36.00

SI.No. Particulars Amount (`)

Mahadev Enterprises, a sole proprietorship firm, opened a shopping complex

1 Intra-state taxable supply within Maharashtra 35,00,000

dealing in supply of goods at multiple locations, i.e. in Himachal Pradesh,

2 Intra-state exempt supply within Maharashtra 2,00,000

Uttarakhand and Tripura in the month of June.

Aggregate turnover 37,00,000

It has furnished the following details relating to the sale made at such multiple

Since the aggregate turnover does not exceed the limit as stated in above provisions locations for the month of June:-

(i.e. ₹ 40 lakhs), he is not required to take registration in the state of Maharashtra Particulars Himachal Uttarakhand Tripura

as per N/N 10/2019. Pradesh

(`) (`) (`)

ii) If Mr. Bajaj also engaged in making inter-state supply, then he cannot avail the

Intra- State supply of taxable goods 22,50,000 - 7,00,000

threshold limit of ₹ 40 lakhs for registration as the benefit is not available to

Intra-State supply of exempted goods 6,00,000

persons making inter-state supply since they are required to take compulsory

Intra-State supply of non-taxable goods - 21,00,000 40,000

registration under section 24 of the said Act. Thus, Mr. Bajaj is required to take

Ch10

registration under GST *Amount excluding GST

iii) The proviso to section 22(1) is applicable to person exclusively engaged in supply With the help of the above mentioned information, answer the following

of goods. Mr. Bajaj is engaged in supply of goods as well as services. Hence the questions giving reasons:-

threshold limit for registration is ₹ 20 lakhs and not ₹ 40 lakhs in FY 2019-20 for (1) Determine whether Mahadev Enterprises is liable to be registered under GST Registration

Mr. Bajaj and thus he has to get registration as his aggregate turnover exceeds ₹ law and what is the threshold limit of taking registration in this case.

20 lakhs in FY 2019-20. (2) Explain with reasons whether your answer in (1) will change in the following

iv) If Mr. Bajaj makes intra-state supply of goods from the states of Telangana then independent cases:

he shall have to apply for registration when the threshold crosses the limit of ₹ 20 (a) If Mahadev Enterprises is dealing in taxable supply of goods only from

lakhs as the benefit of ` 40 lakh is not available to the state Telangana . Himachal Pradesh;

v) The threshold limit of ₹ 40 lakhs is available to person engaged in exclusive supply (b) If Mahadev Enterprises is dealing in taxable supply of goods and services

of goods. However, in case of composite supply of goods, if ancillary services are only from Himachal Pradesh;

provided for making taxable supply of goods then the threshold limit of ₹ 40 lakhs (c) If Mahadev Enterprises is dealing in taxable supply of goods only from

will be available to the person as supply of goods being the principal supply and Himachal Pradesh and has also effected inter - State supplies of

supply of service taxable goods amounting to ` 4,00,000. (CA Final RTP Nov 19)

Answer:- As per section 22 read with Notification No. 10/2019 CT dated 07.03.2019,

a supplier is liable to be registered in the State/ Union territory from where he makes

a taxable supply of goods and/or services, if his aggregate turnover in a financial year

exceeds the threshold limit. The threshold limit for a person making exclusive intra-

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 243

CA Final GST Questioner