Page 19 - Chapter 2.cdr

P. 19

17. Para 5- Supply of services (Renting of Imm. Property, Construction, obligation to refrain from an act , is subject to GST.

Temporary T/f of IPR, Dev etc of software, Agreeing to the obligation 2) Consideration received for non-compete agreement is also consideration for

to refrain from an act etc, t/f of rights supply of services. Consideration of ` 10 lakhs received on the promise of Mr. P CH 2

CCP 02.17.42.00 of not providing similar services to any other person, is consideration for supply

which is chargeable to GST.

(a) M/s. ABC Ltd. provides the following relating to information technology

Since GST is not separately collected, it will be assumed that it is included in

software. Compute the value of taxable service and GST liability (Rate of CGST

` 10 lakhs. Consequently, value of taxable supply will be ` 8,47,458 (i.e., `

9% and SGST 9%)?

10,00,000 × 100 ÷ 118). GST liability on ` 8,47,458 will be calculated as follows

1. Development and Design of information technology software: ` 15 lakhs;

(it will be paid by Mr. P out of his pocket)

2. Sale of pre-packaged software, which is put on media: ` 52 lakhs. Charge of Tax & Concept of Supply

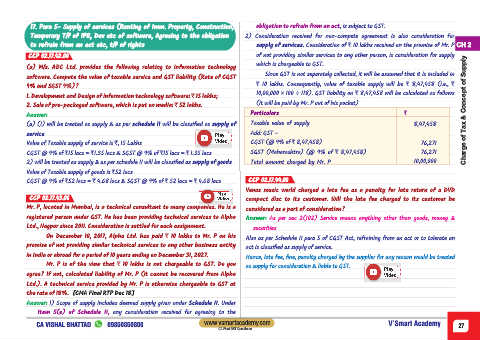

Answer: Particulars `

(a) (1) will be treated as supply & as per schedule II will be classified as supply of Taxable value of supply 8,47,458

service Add: GST –

Value of Taxable supply of service is `, 15 Lakhs CGST (@ 9% of ` 8,47,458) 76,271

CGST @ 9% of `15 lacs = `1.35 lacs & SGST @ 9% of `15 lacs = ` 1.35 lacs SGST (Maharashtra) (@ 9% of ` 8,47,458) 76,271

2) will be treated as supply & as per schedule II will be classified as supply of goods Total amount charged by Mr. P 10,00,000

Value of Taxable supply of goods is `52 lacs

CGST @ 9% of `52 lacs = ` 4.68 lacs & SGST @ 9% of ` 52 lacs = ` 4.68 lacs CCP 02.17.44.00

Venus music world charged a late fee as a penalty for late return of a DVD

CCP 02.17.43.00 compact disc to its customer. Will the late fee charged to its customer be

Mr. P, located in Mumbai, is a technical consultant to many companies. He is a

considered as a part of consideration?

registered person under GST. He has been providing technical services to Alpha

Answer: As per sec 2(102) Service means anything other than goods, money &

Ltd., Nagpur since 2011. Consideration is settled for each assignment.

securities

On December 10, 2017, Alpha Ltd. has paid ` 10 lakhs to Mr. P on his

Also as per Schedule II para 5 of CGST Act, refraining from an act or to tolerate an

promise of not providing similar technical services to any other business entity

act is classified as supply of service.

in India or abroad for a period of 10 years ending on December 31, 2027.

Hence, late fee, fine, penalty charged by the supplier for any reason would be treated

Mr. P is of the view that ` 10 lakhs is not chargeable to GST. Do you

as supply for consideration & liable to GST.

agree? If not, calculated liability of Mr. P (it cannot be recovered from Alpha

Ltd.). A technical service provided by Mr. P is otherwise chargeable to GST at

the rate of 18%. [CMA Final RTP Dec 18]

Answer: 1) Scope of supply includes deemed supply given under Schedule II. Under

Item 5(e) of Schedule II, any consideration received for agreeing to the

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 27

CA Final GST Questioner