Page 24 - Chapter 2.cdr

P. 24

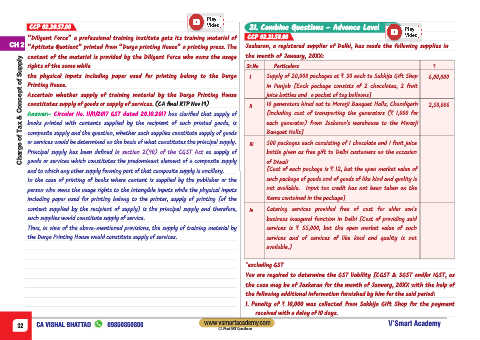

CCP 02.20.57.00 21. Combine Questions - Advance Level

“Diligent Force” a professional training institute gets its training material of CCP 02.21.58.00

CH 2 “Aptitute Quotient” printed from “Durga printing House” a printing press. The Jaskaran, a registered supplier of Delhi, has made the following supplies in

content of the material is provided by the Diligent Force who owns the usage the month of January, 20XX:

Charge of Tax & Concept of Supply

rights of the same while Sr.No Particulars `

the physical inputs including paper used for printing belong to the Durga I Supply of 20,000 packages at ` 30 each to Sukhija Gift Shop 6,00,000

Printing House. in Punjab [Each package consists of 2 chocolates, 2 fruit

Ascertain whether supply of training material by the Durga Printing House juice bottles and a packet of toy balloons]

constitutes supply of goods or supply of services. (CA final RTP Nov 19) ii 10 generators hired out to Morarji Banquet Halls, Chandigarh 2,50,000

Answer:- Circular No. 11/11/2017 GST dated 20.10.2017 has clarified that supply of [including cost of transporting the generators (` 1,000 for

books printed with contents supplied by the recipient of such printed goods, is each generator) from Jaskaran's warehouse to the Morarji

composite supply and the question, whether such supplies constitute supply of goods Banquet Halls]

or services would be determined on the basis of what constitutes the principal supply. iii 500 packages each consisting of 1 chocolate and 1 fruit juice

Principal supply has been defined in section 2(90) of the CGST Act as supply of bottle given as free gift to Delhi customers on the occasion

goods or services which constitutes the predominant element of a composite supply of Diwali

and to which any other supply forming part of that composite supply is ancillary. [Cost of each package is ` 12, but the open market value of

In the case of printing of books where content is supplied by the publisher or the such package of goods and of goods of like kind and quality is

person who owns the usage rights to the intangible inputs while the physical inputs not available. Input tax credit has not been taken on the

including paper used for printing belong to the printer, supply of printing [of the items contained in the package]

content supplied by the recipient of supply] is the principal supply and therefore, iv Catering services provided free of cost for elder son's

such supplies would constitute supply of service. business inaugural function in Delhi [Cost of providing said

Thus, in view of the above-mentioned provisions, the supply of training material by services is ` 55,000, but the open market value of such

the Durga Printing House would constitute supply of services. services and of services of like kind and quality is not

available.]

*excluding GST

You are required to determine the GST liability [CGST & SGST and/or IGST, as

the case may be of Jaskaran for the month of January, 20XX with the help of

the following additional information furnished by him for the said period:

1. Penalty of ` 10,000 was collected from Sukhija Gift Shop for the payment

received with a delay of 10 days.

www.vsmartacademy.com

32 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner