Page 7 - CHAPTER 3 (1).cdr

P. 7

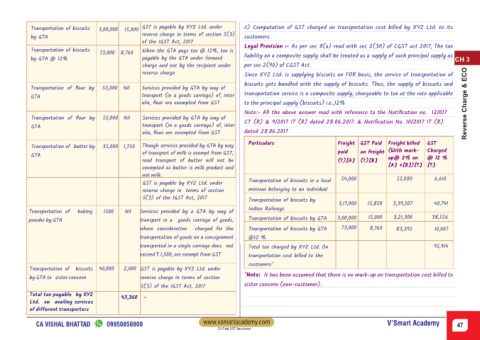

Transportation of biscuits 3,00,000 15,000 GST is payable by XYZ Ltd. under ii) Computation of GST charged on transportation cost billed by XYZ Ltd. to its

reverse charge in terms of section 5(3)

by GTA customers

of the IGST Act, 2017

Legal Provision :- As per sec 8(a) read with sec 2(30) of CGST act 2017, The tax

Transportation of biscuits When the GTA pays tax @ 12%, tax is

73,000 8,760 liability on a composite supply shall be treated as a supply of such principal supply as

by GTA @ 12% payable by the GTA under forward CH 3

charge and not by the recipient under per sec 2(90) of CGST Act.

reverse charge Since XYZ Ltd. is supplying biscuits on FOR basis, the service of transportation of

biscuits gets bundled with the supply of biscuits. Thus, the supply of biscuits and

Transportation of flour by 55,000 Nil Services provided by GTA by way of

GTA transport (in a goods carriage) of, inter transportation service is a composite supply, chargeable to tax at the rate applicable

alia, flour are exempted from GST to the principal supply (biscuits) i.e.,12% Reverse Charge & ECO

Note:- All the above answer read with reference to the Notification no. 12/017

Transportation of flour by 55,000 Nil Services provided by GTA by way of

CT (R) & 9/2017 IT (R) dated 28.06.2017. & Notification No. 10/2017 IT (R)

GTA transport (in a goods carriage) of, inter

alia, flour are exempted from GST dated 28.06.2017

Particulars Freight GST Paid Freight billed GST

Transportation of butter by 35,000 1,750 Though services provided by GTA by way

of transport of milk is exempt from GST, paid on freight (With mark- Charged

GTA

road transport of butter will not be (`)[A] (`)[B] up@ 2% on @ 12 %

[A] +[B])[`] [`]

exempted as butter is milk product and

not milk.

Transportation of biscuits in a local 54,000 55,080 6,610

GST is payable by XYZ Ltd. under

reverse charge in terms of section minivan belonging to an individual

5(3) of the IGST Act, 2017

Transportation of biscuits by

3,17,000 15,850 3,39,507 40,741

Indian Railways

Transportation of baking 1500 Nil Services provided by a GTA by way of

powder by GTA transport in a goods carriage of goods, Transportation of biscuits by GTA 3,00,000 15,000 3,21,300 38,556

where consideration charged for the Transportation of biscuits by GTA 73,000 8,760 83,395 10,007

transportation of goods on a consignment @12 %

transported in a single carriage does not Total tax charged by XYZ Ltd. On 95,914

exceed ` 1,500, are exempt from GST transportation cost billed to the

customers*

Transportation of biscuits 40,000 2,000 GST is payable by XYZ Ltd. under

*Note: It has been assumed that there is no mark-up on transportation cost billed to

by GTA to sister concern reverse charge in terms of section

sister concern (non-customer).

5(3) of the IGST Act, 2017

Total tax payable by XYZ

43,360 -

Ltd. on availing services

of different transporters

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 47

CA Final GST Questioner