Page 21 - 1. COMPILER QB - INDAS 1

P. 21

(ii) Prepare the corrected Balance Sheet & Statement of Profit and Loss.

SOLUTION

On evaluation of the financial statements, following was observed:

1. Reserve for foreseeable loss for INR 500 million, due within 6 months, should be a part of provisions.

Hence it needs to be regrouped, and if it was a part of previous year’s comparatives, a Note should be

added in the notes to account on the regrouping done this year.

2. Interest accrued and due of INR 555 million on term loan will be a part of current liabilities since it is

supposed to be paid within 12 months from the reporting date. Hence, it should be shown under the

heading “Other Current Liabilities”.

3. It can be inferred from Note 3, that the deferred tax liabilities and deferred tax assets relate to taxes on

income levied by the same governing taxation laws, hence these shall be set off, in accordance with AS

22. The net DTA of INR 300 million shall be shown in the balance sheet.

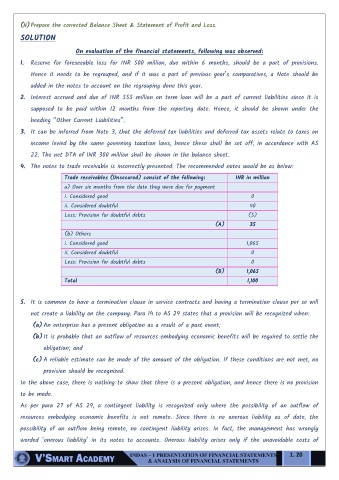

4. The notes to trade receivable is incorrectly presented. The recommended notes would be as below:

Trade receivables (Unsecured) consist of the following: INR in million

a) Over six months from the date they were due for payment

i. Considered good 0

ii. Considered doubtful 40

Less: Provision for doubtful debts (5)

(A) 35

(b) Others

i. Considered good 1,065

ii. Considered doubtful 0

Less: Provision for doubtful debts 0

(B) 1,065

Total 1,100

5. It is common to have a termination clause in service contracts and having a termination clause per se will

not create a liability on the company. Para 14 to AS 29 states that a provision will be recognized when:

(a) An enterprise has a present obligation as a result of a past event;

(b) It is probable that an outflow of resources embodying economic benefits will be required to settle the

obligation; and

(c) A reliable estimate can be made of the amount of the obligation. If these conditions are not met, no

provision should be recognized.

In the above case, there is nothing to show that there is a present obligation, and hence there is no provision

to be made.

As per para 27 of AS 29, a contingent liability is recognized only where the possibility of an outflow of

resources embodying economic benefits is not remote. Since there is no onerous liability as of date, the

possibility of an outflow being remote, no contingent liability arises. In fact, the management has wrongly

worded ‘onerous liability’ in its notes to accounts. Onerous liability arises only if the unavoidable costs of

1. 20