Page 22 - 1. COMPILER QB - INDAS 1

P. 22

meeting the obligation under the contract should exceed the economic benefits expected to be received under

it, which doesn’t seem to be the case as far as Arish Ltd. is concerned. Hence, this note shall be eliminated.

6. The demand notice from the tax department that is under litigation is a clear instance of a ‘contingent

liability’. Accordingly, the note should be revised as –

‘Contingent Liability- Demand notice from income tax department pertaining to INR 6 Million, under

contest with CIT (Appeals) as on the reporting date.

7. The Statement to Profit and Loss needs to represent earnings per share, to be compliant with AS 20.

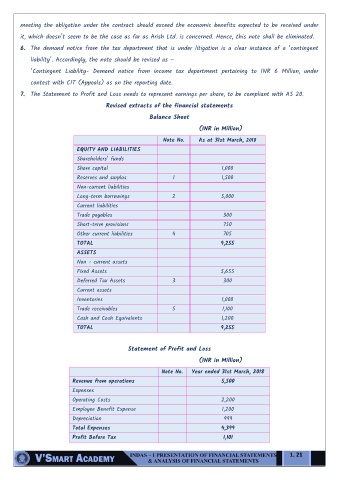

Revised extracts of the financial statements

Balance Sheet

(INR in Million)

Note No. As at 31st March, 2018

EQUITY AND LIABILITIES

Shareholders’ funds

Share capital 1,000

Reserves and surplus 1 1,500

Non-current liabilities

Long-term borrowings 2 5,000

Current liabilities

Trade payables 300

Short-term provisions 750

Other current liabilities 4 705

TOTAL 9,255

ASSETS

Non - current assets

Fixed Assets 5,655

Deferred Tax Assets 3 300

Current assets

Inventories 1,000

Trade receivables 5 1,100

Cash and Cash Equivalents 1,200

TOTAL 9,255

Statement of Profit and Loss

(INR in Million)

Note No. Year ended 31st March, 2018

Revenue from operations 5,500

Expenses

Operating Costs 2,200

Employee Benefit Expense 1,200

Depreciation 999

Total Expenses 4,399

Profit Before Tax 1,101

1. 21