Page 3 - 1. COMPILER QB - INDAS 1

P. 3

Hence, the liability should be classified as current in the financial statement for the year ended March 31,

20X2.

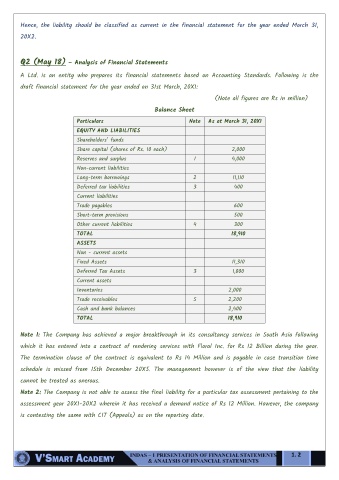

Q2 (May 18) – Analysis of Financial Statements

A Ltd. is an entity who prepares its financial statements based on Accounting Standards. Following is the

draft financial statement for the year ended on 31st March, 20X1:

(Note all figures are Rs in million)

Balance Sheet

Particulars Note As at March 31, 20X1

EQUITY AND LIABILITIES

Shareholders’ funds

Share capital (shares of Rs. 10 each) 2,000

Reserves and surplus 1 4,000

Non-current liabilities

Long-term borrowings 2 11,110

Deferred tax liabilities 3 400

Current liabilities

Trade payables 600

Short-term provisions 500

Other current liabilities 4 300

TOTAL 18,910

ASSETS

Non - current assets

Fixed Assets 11,310

Deferred Tax Assets 3 1,000

Current assets

Inventories 2,000

Trade receivables 5 2,200

Cash and bank balances 2,400

TOTAL 18,910

Note 1: The Company has achieved a major breakthrough in its consultancy services in South Asia following

which it has entered into a contract of rendering services with Floral Inc. for Rs 12 Billion during the year.

The termination clause of the contract is equivalent to Rs 14 Million and is payable in case transition time

schedule is missed from 15th December 20X5. The management however is of the view that the liability

cannot be treated as onerous.

Note 2: The Company is not able to assess the final liability for a particular tax assessment pertaining to the

assessment year 20X1-20X2 wherein it has received a demand notice of Rs 12 Million. However, the company

is contesting the same with CIT (Appeals) as on the reporting date.

1. 2