Page 19 - 2. COMPILER QB - INDAS 12

P. 19

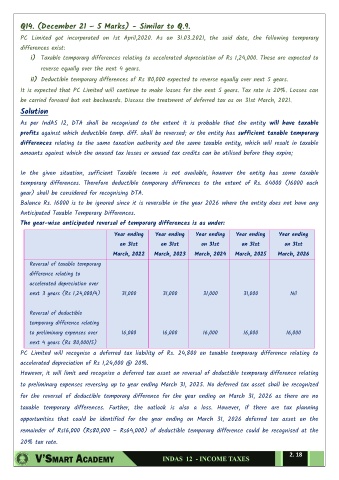

Q14. (December 21 – 5 Marks) - Similar to Q.9.

PC Limited got incorporated on 1st April,2020. As on 31.03.2021, the said date, the following temporary

differences exist:

i) Taxable temporary differences relating to accelerated depreciation of Rs 1,24,000. These are expected to

reverse equally over the next 4 years.

ii) Deductible temporary differences of Rs 80,000 expected to reverse equally over next 5 years.

It is expected that PC Limited will continue to make losses for the next 5 years. Tax rate is 20%. Losses can

be carried forward but not backwards. Discuss the treatment of deferred tax as on 31st March, 2021.

Solution

As per IndAS 12, DTA shall be recognised to the extent it is probable that the entity will have taxable

profits against which deductible temp. diff. shall be reversed; or the entity has sufficient taxable temporary

differences relating to the same taxation authority and the same taxable entity, which will result in taxable

amounts against which the unused tax losses or unused tax credits can be utilised before they expire;

In the given situation, sufficient Taxable Income is not available, however the entity has some taxable

temporary differences. Therefore deductible temporary differences to the extent of Rs. 64000 (16000 each

year) shall be considered for recognising DTA.

Balance Rs. 16000 is to be ignored since it is reversible in the year 2026 where the entity does not have any

Anticipated Taxable Temporary Differences.

The year-wise anticipated reversal of temporary differences is as under:

Year ending Year ending Year ending Year ending Year ending

on 31st on 31st on 31st on 31st on 31st

March, 2022 March, 2023 March, 2024 March, 2025 March, 2026

Reversal of taxable temporary

difference relating to

accelerated depreciation over

next 3 years (Rs 1,24,000/4) 31,000 31,000 31,000 31,000 Nil

Reversal of deductible

temporary difference relating

to preliminary expenses over 16,000 16,000 16,000 16,000 16,000

next 4 years (Rs 80,000/5)

PC Limited will recognise a deferred tax liability of Rs. 24,800 on taxable temporary difference relating to

accelerated depreciation of Rs 1,24,000 @ 20%.

However, it will limit and recognise a deferred tax asset on reversal of deductible temporary difference relating

to preliminary expenses reversing up to year ending March 31, 2025. No deferred tax asset shall be recognized

for the reversal of deductible temporary difference for the year ending on March 31, 2026 as there are no

taxable temporary differences. Further, the outlook is also a loss. However, if there are tax planning

opportunities that could be identified for the year ending on March 31, 2026 deferred tax asset on the

remainder of Rs16,000 (Rs80,000 – Rs64,000) of deductible temporary difference could be recognised at the

20% tax rate.

2. 18