Page 15 - 2. COMPILER QB - INDAS 12

P. 15

The difference of Rs. 4,688 would reverse in future years when depreciation for accounting purposes would be

higher as compared to depreciation for tax purposes because depreciation for accounting purposes would be

computed on higher carrying amount of property, plant and equipment as compared to carrying amount of

those assets for tax purposes.

Alternate answer

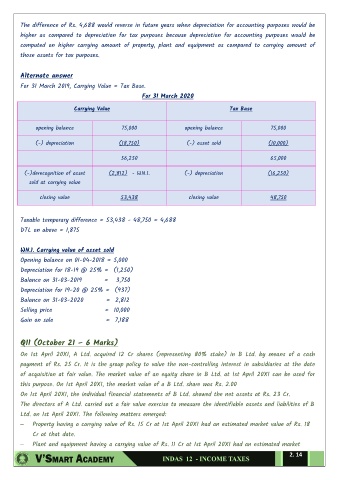

For 31 March 2019, Carrying Value = Tax Base.

For 31 March 2020

Carrying Value Tax Base

opening balance 75,000 opening balance 75,000

(-) depreciation (18,750) (-) asset sold (10,000)

56,250 65,000

(-)derecognition of asset (2,812) - WN.1. (-) depreciation (16,250)

sold at carrying value

closing value 53,438 closing value 48,750

Taxable temporary difference = 53,438 - 48,750 = 4,688

DTL on above = 1,875

WN.1. Carrying value of asset sold

Opening balance on 01-04-2018 = 5,000

Depreciation for 18-19 @ 25% = (1,250)

Balance on 31-03-2019 = 3,750

Depreciation for 19-20 @ 25% = (937)

Balance on 31-03-2020 = 2,812

Selling price = 10,000

Gain on sale = 7,188

Q11 (October 21 – 6 Marks)

On 1st April 20X1, A Ltd. acquired 12 Cr shares (representing 80% stake) in B Ltd. by means of a cash

payment of Rs. 25 Cr. It is the group policy to value the non-controlling interest in subsidiaries at the date

of acquisition at fair value. The market value of an equity share in B Ltd. at 1st April 20X1 can be used for

this purpose. On 1st April 20X1, the market value of a B Ltd. share was Rs. 2.00

On 1st April 20X1, the individual financial statements of B Ltd. showed the net assets at Rs. 23 Cr.

The directors of A Ltd. carried out a fair value exercise to measure the identifiable assets and liabilities of B

Ltd. on 1st April 20X1. The following matters emerged:

– Property having a carrying value of Rs. 15 Cr at 1st April 20X1 had an estimated market value of Rs. 18

Cr at that date.

– Plant and equipment having a carrying value of Rs. 11 Cr at 1st April 20X1 had an estimated market

2. 14