Page 20 - 2. COMPILER QB - INDAS 12

P. 20

NEWLY ADDED QUESTIONS IN ICAI MODULE

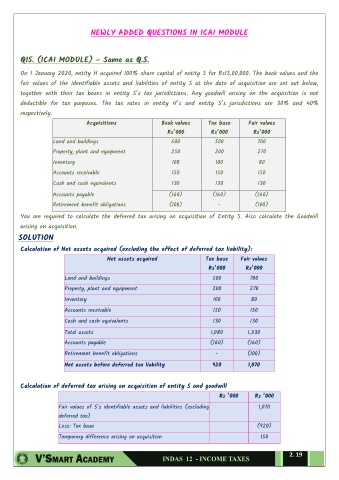

Q15. (ICAI MODULE) - Same as Q.5.

On 1 January 2020, entity H acquired 100% share capital of entity S for Rs15,00,000. The book values and the

fair values of the identifiable assets and liabilities of entity S at the date of acquisition are set out below,

together with their tax bases in entity S’s tax jurisdictions. Any goodwill arising on the acquisition is not

deductible for tax purposes. The tax rates in entity H’s and entity S’s jurisdictions are 30% and 40%

respectively.

Acquisitions Book values Tax base Fair values

Rs’000 Rs’000 Rs’000

Land and buildings 600 500 700

Property, plant and equipment 250 200 270

Inventory 100 100 80

Accounts receivable 150 150 150

Cash and cash equivalents 130 130 130

Accounts payable (160) (160) (160)

Retirement benefit obligations (100) - (100)

You are required to calculate the deferred tax arising on acquisition of Entity S. Also calculate the Goodwill

arising on acquisition.

SOLUTION

Calculation of Net assets acquired (excluding the effect of deferred tax liability):

Net assets acquired Tax base Fair values

Rs’000 Rs’000

Land and buildings 500 700

Property, plant and equipment 200 270

Inventory 100 80

Accounts receivable 150 150

Cash and cash equivalents 130 130

Total assets 1,080 1,330

Accounts payable (160) (160)

Retirement benefit obligations - (100)

Net assets before deferred tax liability 920 1,070

Calculation of deferred tax arising on acquisition of entity S and goodwill

Rs ’000 Rs ’000

Fair values of S’s identifiable assets and liabilities (excluding 1,070

deferred tax)

Less: Tax base (920)

Temporary difference arising on acquisition 150

2. 19