Page 28 - 16. COMPILER QB - INDAS 103

P. 28

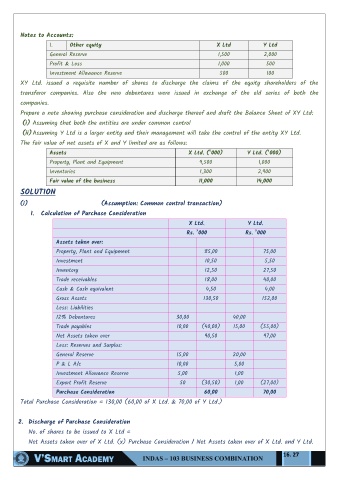

Notes to Accounts:

1. Other equity X Ltd Y Ltd

General Reserve 1,500 2,000

Profit & Loss 1,000 500

Investment Allowance Reserve 500 100

XY Ltd. issued a requisite number of shares to discharge the claims of the equity shareholders of the

transferor companies. Also the new debentures were issued in exchange of the old series of both the

companies.

Prepare a note showing purchase consideration and discharge thereof and draft the Balance Sheet of XY Ltd:

(i) Assuming that both the entities are under common control

(ii) Assuming Y Ltd is a larger entity and their management will take the control of the entity XY Ltd.

The fair value of net assets of X and Y limited are as follows:

Assets X Ltd. (‘000) Y Ltd. (‘000)

Property, Plant and Equipment 9,500 1,000

Inventories 1,300 2,900

Fair value of the business 11,000 14,000

SOLUTION

(i) (Assumption: Common control transaction)

1. Calculation of Purchase Consideration

X Ltd. Y Ltd.

Rs. ’000 Rs. ’000

Assets taken over:

Property, Plant and Equipment 85,00 75,00

Investment 10,50 5,50

Inventory 12,50 27,50

Trade receivables 18,00 40,00

Cash & Cash equivalent 4,50 4,00

Gross Assets 130,50 152,00

Less: Liabilities

12% Debentures 30,00 40,00

Trade payables 10,00 (40,00) 15,00 (55,00)

Net Assets taken over 90,50 97,00

Less: Reserves and Surplus:

General Reserve 15,00 20,00

P & L A/c 10,00 5,00

Investment Allowance Reserve 5,00 1,00

Export Profit Reserve 50 (30,50) 1,00 (27,00)

Purchase Consideration 60,00 70,00

Total Purchase Consideration = 130,00 (60,00 of X Ltd. & 70,00 of Y Ltd.)

2. Discharge of Purchase Consideration

No. of shares to be issued to X Ltd =

Net Assets taken over of X Ltd. (x) Purchase Consideration / Net Assets taken over of X Ltd. and Y Ltd.

16. 27