Page 30 - 16. COMPILER QB - INDAS 103

P. 30

❖ The total purchase consideration is to be discharged by XY Ltd. in such a way that the rights of the

shareholders of X Ltd. and Y Ltd. remain unaltered in the future profits of XY Ltd.

(ii) Assuming Y Ltd is a larger entity and their management will take the control of the entity XY

Ltd.

In this case Y Ltd. and X Ltd. are not under common control and hence accounting prescribed under Ind AS

103 for business combination will be applied. A question arises here is who is the accounting acquirer XY Ltd

which is issuing the shares or X Ltd. or Y Ltd. As per the accounting guidance provided in Ind AS 103,

sometimes the legal acquirer may not be the accounting acquirer. In the given scenario, although XY Ltd. is

issuing the shares but Y Ltd. post-merger will have control and is bigger in size which is a clear indicator that

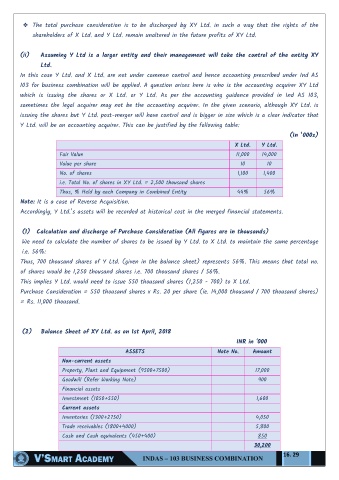

Y Ltd. will be an accounting acquirer. This can be justified by the following table:

(In ‘000s)

X Ltd. Y Ltd.

Fair Value 11,000 14,000

Value per share 10 10

No. of shares 1,100 1,400

i.e. Total No. of shares in XY Ltd. = 2,500 thousand shares

Thus, % Held by each Company in Combined Entity 44% 56%

Note: It is a case of Reverse Acquisition.

Accordingly, Y Ltd.‖s assets will be recorded at historical cost in the merged financial statements.

(1) Calculation and discharge of Purchase Consideration (All figures are in thousands)

We need to calculate the number of shares to be issued by Y Ltd. to X Ltd. to maintain the same percentage

i.e. 56%:

Thus, 700 thousand shares of Y Ltd. (given in the balance sheet) represents 56%. This means that total no.

of shares would be 1,250 thousand shares i.e. 700 thousand shares / 56%.

This implies Y Ltd. would need to issue 550 thousand shares (1,250 - 700) to X Ltd.

Purchase Consideration = 550 thousand shares x Rs. 20 per share (ie. 14,000 thousand / 700 thousand shares)

= Rs. 11,000 thousand.

(2) Balance Sheet of XY Ltd. as on 1st April, 2018

INR in '000

ASSETS Note No. Amount

Non-current assets

Property, Plant and Equipment (9500+7500) 17,000

Goodwill (Refer Working Note) 900

Financial assets

Investment (1050+550) 1,600

Current assets

Inventories (1300+2750) 4,050

Trade receivables (1800+4000) 5,800

Cash and Cash equivalents (450+400) 850

30,200

16. 29