Page 29 - 16. COMPILER QB - INDAS 103

P. 29

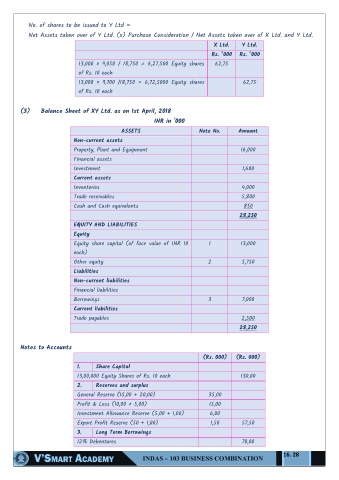

No. of shares to be issued to Y Ltd =

Net Assets taken over of Y Ltd. (x) Purchase Consideration / Net Assets taken over of X Ltd. and Y Ltd.

X Ltd. Y Ltd.

Rs. ’000 Rs. ’000

13,000 × 9,050 / 18,750 = 6,27,500 Equity shares 62,75

of Rs. 10 each

13,000 × 9,700 /18,750 = 6,72,5000 Equity shares 62,75

of Rs. 10 each

(3) Balance Sheet of XY Ltd. as on 1st April, 2018

INR in '000

ASSETS Note No. Amount

Non-current assets

Property, Plant and Equipment 16,000

Financial assets

Investment 1,600

Current assets

Inventories 4,000

Trade receivables 5,800

Cash and Cash equivalents 850

28,250

EQUITY AND LIABILITIES

Equity

Equity share capital (of face value of INR 10 1 13,000

each)

Other equity 2 5,750

Liabilities

Non-current liabilities

Financial liabilities

Borrowings 3 7,000

Current liabilities

Trade payables 2,500

28,250

Notes to Accounts

(Rs. 000) (Rs. 000)

1. Share Capital

13,00,000 Equity Shares of Rs. 10 each 130,00

2. Reserves and surplus

General Reserve (15,00 + 20,00) 35,00

Profit & Loss (10,00 + 5,00) 15,00

Investment Allowance Reserve (5,00 + 1,00) 6,00

Export Profit Reserve (50 + 1,00) 1,50 57,50

3. Long Term Borrowings

12% Debentures 70,00

16. 28