Page 3 - 19. COMPILER QB - INDAS 115

P. 3

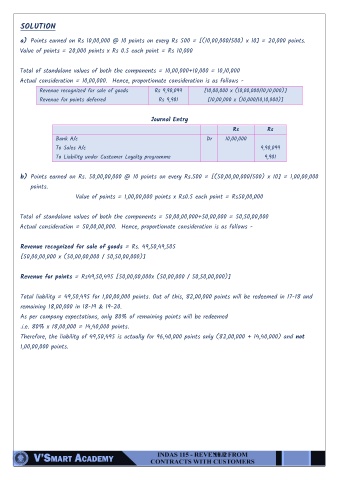

SOLUTION

a) Points earned on Rs 10,00,000 @ 10 points on every Rs 500 = [(10,00,000/500) x 10] = 20,000 points.

Value of points = 20,000 points x Rs 0.5 each point = Rs 10,000

Total of standalone values of both the components = 10,00,000+10,000 = 10,10,000

Actual consideration = 10,00,000. Hence, proportionate consideration is as follows -

Revenue recognized for sale of goods Rs 9,90,099 [10,00,000 x (10,00,000/10,10,000)]

Revenue for points deferred Rs 9,901 [10,00,000 x (10,000/10,10,000)]

Journal Entry

Rs Rs

Bank A/c Dr 10,00,000

To Sales A/c 9,90,099

To Liability under Customer Loyalty programme 9,901

b) Points earned on Rs. 50,00,00,000 @ 10 points on every Rs.500 = [(50,00,00,000/500) x 10] = 1,00,00,000

points.

Value of points = 1,00,00,000 points x Rs0.5 each point = Rs50,00,000

Total of standalone values of both the components = 50,00,00,000+50,00,000 = 50,50,00,000

Actual consideration = 50,00,00,000. Hence, proportionate consideration is as follows -

Revenue recognized for sale of goods = Rs. 49,50,49,505

[50,00,00,000 x (50,00,00,000 / 50,50,00,000)]

Revenue for points = Rs49,50,495 [50,00,00,000x (50,00,000 / 50,50,00,000)]

Total liability = 49,50,495 for 1,00,00,000 points. Out of this, 82,00,000 points will be redeemed in 17-18 and

remaining 18,00,000 in 18-19 & 19-20.

As per company expectations, only 80% of remaining points will be redeemed

.i.e. 80% x 18,00,000 = 14,40,000 points.

Therefore, the liability of 49,50,495 is actually for 96,40,000 points only (82,00,000 + 14,40,000) and not

1,00,00,000 points.

19. 2