Page 35 - 19. COMPILER QB - INDAS 115

P. 35

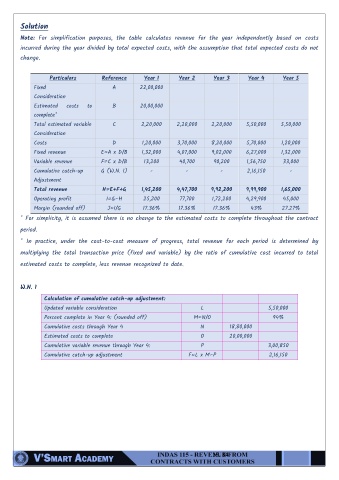

Solution

Note: For simplification purposes, the table calculates revenue for the year independently based on costs

incurred during the year divided by total expected costs, with the assumption that total expected costs do not

change.

Particulars Reference Year 1 Year 2 Year 3 Year 4 Year 5

Fixed A 22,00,000

Consideration

Estimated costs to B 20,00,000

complete*

Total estimated variable C 2,20,000 2,20,000 2,20,000 5,50,000 5,50,000

Consideration

Costs D 1,20,000 3,70,000 8,20,000 5,70,000 1,20,000

Fixed revenue E=A x D/B 1,32,000 4,07,000 9,02,000 6,27,000 1,32,000

Variable revenue F=C x D/B 13,200 40,700 90,200 1,56,750 33,000

Cumulative catch-up G (W.N. 1) - - - 2,16,150 -

Adjustment

Total revenue H=E+F+G 1,45,200 4,47,700 9,92,200 9,99,900 1,65,000

Operating profit I=G–H 25,200 77,700 1,72,200 4,29,900 45,000

Margin (rounded off) J=I/G 17.36% 17.36% 17.36% 43% 27.27%

* For simplicity, it is assumed there is no change to the estimated costs to complete throughout the contract

period.

* In practice, under the cost-to-cost measure of progress, total revenue for each period is determined by

multiplying the total transaction price (fixed and variable) by the ratio of cumulative cost incurred to total

estimated costs to complete, less revenue recognized to date.

W.N. 1

Calculation of cumulative catch-up adjustment:

Updated variable consideration L 5,50,000

Percent complete in Year 4: (rounded off) M=N/O 94%

Cumulative costs through Year 4 N 18,80,000

Estimated costs to complete O 20,00,000

Cumulative variable revenue through Year 4: P 3,00,850

Cumulative catch-up adjustment F=L x M–P 2,16,150

19. 34