Page 30 - 19. COMPILER QB - INDAS 115

P. 30

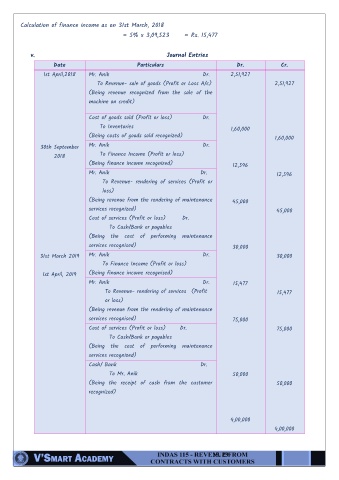

Calculation of finance income as on 31st March, 2018

= 5% x 3,09,523 = Rs. 15,477

v. Journal Entries

Date Particulars Dr. Cr.

1st April,2018 Mr. Anik Dr. 2,51,927

To Revenue- sale of goods (Profit or Loss A/c) 2,51,927

(Being revenue recognized from the sale of the

machine on credit)

Cost of goods sold (Profit or loss) Dr.

To Inventories

1,60,000

(Being costs of goods sold recognized)

1,60,000

Mr. Anik Dr.

30th September

2018 To Finance Income (Profit or loss)

(Being finance income recognized) 12,596

Mr. Anik Dr. 12,596

To Revenue- rendering of services (Profit or

loss)

(Being revenue from the rendering of maintenance 45,000

services recognized) 45,000

Cost of services (Profit or loss) Dr.

To Cash/Bank or payables

(Being the cost of performing maintenance

services recognised) 30,000

31st March 2019 Mr. Anik Dr. 30,000

To Finance Income (Profit or loss)

1st April, 2019 (Being finance income recognised)

Mr. Anik Dr. 15,477

To Revenue- rendering of services (Profit 15,477

or loss)

(Being revenue from the rendering of maintenance

services recognised) 75,000

Cost of services (Profit or loss) Dr. 75,000

To Cash/Bank or payables

(Being the cost of performing maintenance

services recognized)

Cash/ Bank Dr.

To Mr. Anik 50,000

(Being the receipt of cash from the customer 50,000

recognized)

4,00,000

4,00,000

19. 29