Page 16 - 21. COMPILER QB - INDAS 33

P. 16

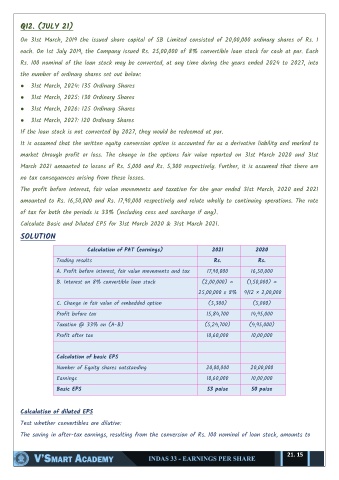

Q12. (JULY 21)

On 31st March, 2019 the issued share capital of SB Limited consisted of 20,00,000 ordinary shares of Rs. 1

each. On 1st July 2019, the Company issued Rs. 25,00,000 of 8% convertible loan stock for cash at par. Each

Rs. 100 nominal of the loan stock may be converted, at any time during the years ended 2024 to 2027, into

the number of ordinary shares set out below:

● 31st March, 2024: 135 Ordinary Shares

● 31st March, 2025: 130 Ordinary Shares

● 31st March, 2026: 125 Ordinary Shares

● 31st March, 2027: 120 Ordinary Shares

If the loan stock is not converted by 2027, they would be redeemed at par.

It is assumed that the written equity conversion option is accounted for as a derivative liability and marked to

market through profit or loss. The change in the options fair value reported on 31st March 2020 and 31st

March 2021 amounted to losses of Rs. 5,000 and Rs. 5,300 respectively. Further, it is assumed that there are

no tax consequences arising from these losses.

The profit before interest, fair value movements and taxation for the year ended 31st March, 2020 and 2021

amounted to Rs. 16,50,000 and Rs. 17,90,000 respectively and relate wholly to continuing operations. The rate

of tax for both the periods is 33% (including cess and surcharge if any).

Calculate Basic and Diluted EPS for 31st March 2020 & 31st March 2021.

SOLUTION

Calculation of PAT (earnings) 2021 2020

Trading results Rs. Rs.

A. Profit before interest, fair value movements and tax 17,90,000 16,50,000

B. Interest on 8% convertible loan stock (2,00,000) = (1,50,000) =

25,00,000 x 8% 9/12 × 2,00,000

C. Change in fair value of embedded option (5,300) (5,000)

Profit before tax 15,84,700 14,95,000

Taxation @ 33% on (A-B) (5,24,700) (4,95,000)

Profit after tax 10,60,000 10,00,000

Calculation of basic EPS

Number of Equity shares outstanding 20,00,000 20,00,000

Earnings 10,60,000 10,00,000

Basic EPS 53 paise 50 paise

Calculation of diluted EPS

Test whether convertibles are dilutive:

The saving in after-tax earnings, resulting from the conversion of Rs. 100 nominal of loan stock, amounts to

21. 15