Page 13 - 21. COMPILER QB - INDAS 33

P. 13

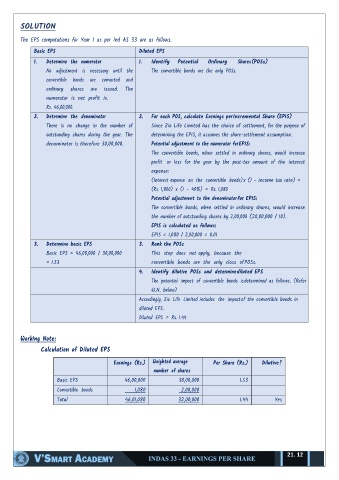

SOLUTION

The EPS computations for Year 1 as per Ind AS 33 are as follows.

Basic EPS Diluted EPS

1. Determine the numerator 1. Identify Potential Ordinary Shares (POSs)

No adjustment is necessary until the The convertible bonds are the only POSs.

convertible bonds are converted and

ordinary shares are issued. The

numerator is net profit ie.

Rs. 46,00,000.

2. Determine the denominator 2. For each POS, calculate Earnings per Incremental Share (EPIS)

There is no change in the number of Since Zio Life Limited has the choice of settlement, for the purpose of

outstanding shares during the year. The determining the EPIS, it assumes the share-settlement assumption.

denominator is therefore 30,00,000. Potential adjustment to the numerator for EPIS:

The convertible bonds, when settled in ordinary shares, would increase

profit or loss for the year by the post-tax amount of the interest

expense:

(Interest expense on the convertible bonds) x (1 - income tax rate) =

(Rs. 1,800) x (1 - 40%) = Rs. 1,080

Potential adjustment to the denominator for EPIS:

The convertible bonds, when settled in ordinary shares, would increase

the number of outstanding shares by 2,00,000 (20,00,000 / 10).

EPIS is calculated as follows:

EPIS = 1,080 / 2,00,000 = 0.01

3. Determine basic EPS 3. Rank the POSs

Basic EPS = 46,00,000 / 30,00,000 This step does not apply, because the

= 1.53 convertible bonds are the only class of POSs.

4. Identify dilutive POSs and determine diluted EPS

The potential impact of convertible bonds is determined as follows. (Refer

W.N. below)

Accordingly, Zio Life Limited includes the impact of the convertible bonds in

diluted EPS.

Diluted EPS = Rs. 1.44

Working Note:

Calculation of Diluted EPS

Earnings (Rs.) Weighted average Per Share (Rs.) Dilutive?

number of shares

Basic EPS 46,00,000 30,00,000 1.53

Convertible bonds 1,080 2,00,000

Total 46,01,080 32,00,000 1.44 Yes

21. 12