Page 15 - 21. COMPILER QB - INDAS 33

P. 15

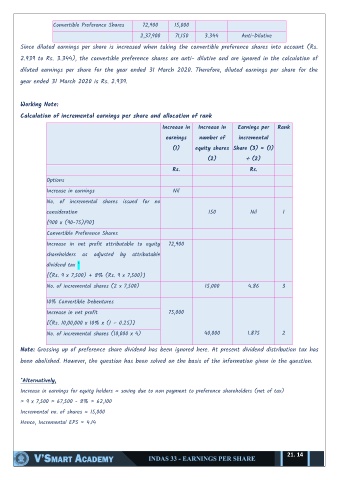

Convertible Preference Shares 72,900 15,000

2,37,900 71,150 3.344 Anti-Dilutive

Since diluted earnings per share is increased when taking the convertible preference shares into account (Rs.

2.939 to Rs. 3.344), the convertible preference shares are anti- dilutive and are ignored in the calculation of

diluted earnings per share for the year ended 31 March 2020. Therefore, diluted earnings per share for the

year ended 31 March 2020 is Rs. 2.939.

Working Note:

Calculation of incremental earnings per share and allocation of rank

Increase in Increase in Earnings per Rank

earnings number of incremental

(1) equity shares Share (3) = (1)

(2) ÷ (2)

Rs. Rs.

Options

Increase in earnings Nil

No. of incremental shares issued for no

consideration 150 Nil 1

[900 x (90-75)/90]

Convertible Preference Shares

Increase in net profit attributable to equity 72,900

shareholders as adjusted by attributable

dividend tax *

[(Rs. 9 x 7,500) + 8% (Rs. 9 x 7,500)]

No. of incremental shares (2 x 7,500) 15,000 4.86 3

10% Convertible Debentures

Increase in net profit 75,000

[(Rs. 10,00,000 x 10% x (1 – 0.25)]

No. of incremental shares (10,000 x 4) 40,000 1.875 2

Note: Grossing up of preference share dividend has been ignored here. At present dividend distribution tax has

been abolished. However, the question has been solved on the basis of the information given in the question.

*Alternatively,

Increase in earnings for equity holders = saving due to non payment to preference shareholders (net of tax)

= 9 x 7,500 = 67,500 - 8% = 62,100

Incremental no. of shares = 15,000

Hence, Incremental EPS = 4.14

21. 14