Page 14 - 27. COMPILER QB - IND AS 7

P. 14

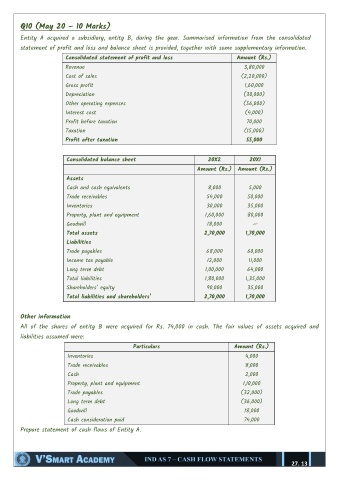

Q10 (May 20 – 10 Marks)

Entity A acquired a subsidiary, entity B, during the year. Summarised information from the consolidated

statement of profit and loss and balance sheet is provided, together with some supplementary information.

Consolidated statement of profit and loss Amount (Rs.)

Revenue 3,80,000

Cost of sales (2,20,000)

Gross profit 1,60,000

Depreciation (30,000)

Other operating expenses (56,000)

Interest cost (4,000)

Profit before taxation 70,000

Taxation (15,000)

Profit after taxation 55,000

Consolidated balance sheet 20X2 20X1

Amount (Rs.) Amount (Rs.)

Assets

Cash and cash equivalents 8,000 5,000

Trade receivables 54,000 50,000

Inventories 30,000 35,000

Property, plant and equipment 1,60,000 80,000

Goodwill 18,000 —

Total assets 2,70,000 1,70,000

Liabilities

Trade payables 68,000 60,000

Income tax payable 12,000 11,000

Long term debt 1,00,000 64,000

Total liabilities 1,80,000 1,35,000

Shareholders‖ equity 90,000 35,000

Total liabilities and shareholders’ 2,70,000 1,70,000

Other information

All of the shares of entity B were acquired for Rs. 74,000 in cash. The fair values of assets acquired and

liabilities assumed were:

Particulars Amount (Rs.)

Inventories 4,000

Trade receivables 8,000

Cash 2,000

Property, plant and equipment 1,10,000

Trade payables (32,000)

Long term debt (36,000)

Goodwill 18,000

Cash consideration paid 74,000

Prepare statement of cash flows of Entity A.

27. 13