Page 15 - 27. COMPILER QB - IND AS 7

P. 15

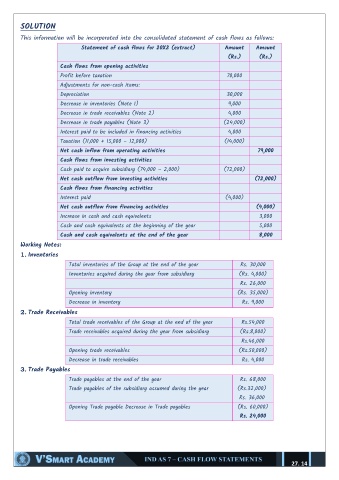

SOLUTION

This information will be incorporated into the consolidated statement of cash flows as follows:

Statement of cash flows for 20X2 (extract) Amount Amount

(Rs.) (Rs.)

Cash flows from opening activities

Profit before taxation 70,000

Adjustments for non-cash items:

Depreciation 30,000

Decrease in inventories (Note 1) 9,000

Decrease in trade receivables (Note 2) 4,000

Decrease in trade payables (Note 3) (24,000)

Interest paid to be included in financing activities 4,000

Taxation (11,000 + 15,000 – 12,000) (14,000)

Net cash inflow from operating activities 79,000

Cash flows from investing activities

Cash paid to acquire subsidiary (74,000 – 2,000) (72,000)

Net cash outflow from investing activities (72,000)

Cash flows from financing activities

Interest paid (4,000)

Net cash outflow from financing activities (4,000)

Increase in cash and cash equivalents 3,000

Cash and cash equivalents at the beginning of the year 5,000

Cash and cash equivalents at the end of the year 8,000

Working Notes:

1. Inventories

Total inventories of the Group at the end of the year Rs. 30,000

Inventories acquired during the year from subsidiary (Rs. 4,000)

Rs. 26,000

Opening inventory (Rs. 35,000)

Decrease in inventory Rs. 9,000

2. Trade Receivables

Total trade receivables of the Group at the end of the year Rs.54,000

Trade receivables acquired during the year from subsidiary (Rs.8,000)

Rs.46,000

Opening trade receivables (Rs.50,000)

Decrease in trade receivables Rs. 4,000

3. Trade Payables

Trade payables at the end of the year Rs. 68,000

Trade payables of the subsidiary assumed during the year (Rs.32,000)

Rs. 36,000

Opening Trade payable Decrease in Trade payables (Rs. 60,000)

Rs. 24,000

27. 14