Page 5 - 27. COMPILER QB - IND AS 7

P. 5

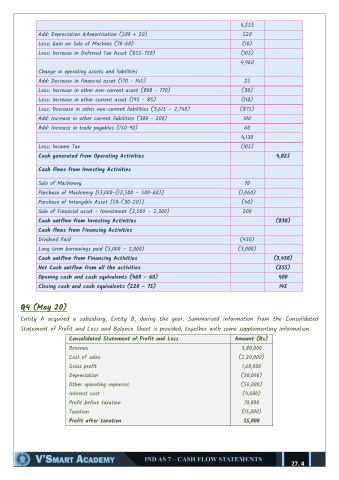

4,555

Add: Depreciation &Amortisation (500 + 20) 520

Less: Gain on Sale of Machine (70-60) (10)

Less: Increase in Deferred Tax Asset (855-750) (105)

4,960

Change in operating assets and liabilities

Add: Decrease in financial asset (170 - 145) 25

Less: Increase in other non-current asset (800 - 770) (30)

Less: Increase in other current asset (195 - 85) (110)

Less: Decrease in other non-current liabilities (3,615 – 2,740) (875)

Add: Increase in other current liabilities (300 - 200) 100

Add: Increase in trade payables (150-90) 60

4,130

Less: Income Tax (105)

Cash generated from Operating Activities 4,025

Cash flows from Investing Activities

Sale of Machinery 70

Purchase of Machinery [13,000-(12,500 – 500-60)] (1,060)

Purchase of Intangible Asset [50-(30-20)] (40)

Sale of Financial asset - Investment (2,500 – 2,300) 200

Cash outflow from Investing Activities (830)

Cash flows from Financing Activities

Dividend Paid (450)

Long term borrowings paid (5,000 – 2,000) (3,000)

Cash outflow from Financing Activities (3,450)

Net Cash outflow from all the activities (255)

Opening cash and cash equivalents (460 – 60) 400

Closing cash and cash equivalents (220 – 75) 145

Q4 (May 20)

Entity A acquired a subsidiary, Entity B, during the year. Summarised information from the Consolidated

Statement of Profit and Loss and Balance Sheet is provided, together with some supplementary information.

Consolidated Statement of Profit and Loss Amount (Rs)

Revenue 3,80,000

Cost of sales (2,20,000)

Gross profit 1,60,000

Depreciation (30,000)

Other operating expenses (56,000)

Interest cost (4,000)

Profit before taxation 70,000

Taxation (15,000)

Profit after taxation 55,000

27. 4