Page 8 - 27. COMPILER QB - IND AS 7

P. 8

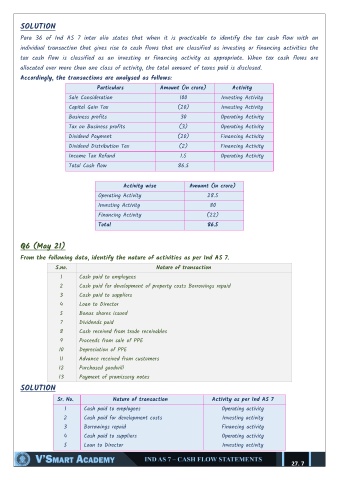

SOLUTION

Para 36 of Ind AS 7 inter alia states that when it is practicable to identify the tax cash flow with an

individual transaction that gives rise to cash flows that are classified as investing or financing activities the

tax cash flow is classified as an investing or financing activity as appropriate. When tax cash flows are

allocated over more than one class of activity, the total amount of taxes paid is disclosed.

Accordingly, the transactions are analysed as follows:

Particulars Amount (in crore) Activity

Sale Consideration 100 Investing Activity

Capital Gain Tax (20) Investing Activity

Business profits 30 Operating Activity

Tax on Business profits (3) Operating Activity

Dividend Payment (20) Financing Activity

Dividend Distribution Tax (2) Financing Activity

Income Tax Refund 1.5 Operating Activity

Total Cash flow 86.5

Activity wise Amount (in crore)

Operating Activity 28.5

Investing Activity 80

Financing Activity (22)

Total 86.5

Q6 (May 21)

From the following data, identify the nature of activities as per Ind AS 7.

S.no. Nature of transaction

1 Cash paid to employees

2 Cash paid for development of property costs Borrowings repaid

3 Cash paid to suppliers

4 Loan to Director

5 Bonus shares issued

7 Dividends paid

8 Cash received from trade receivables

9 Proceeds from sale of PPE

10 Depreciation of PPE

11 Advance received from customers

12 Purchased goodwill

13 Payment of promissory notes

SOLUTION

Sr. No. Nature of transaction Activity as per Ind AS 7

1 Cash paid to employees Operating activity

2 Cash paid for development costs Investing activity

3 Borrowings repaid Financing activity

4 Cash paid to suppliers Operating activity

5 Loan to Director Investing activity

27. 7