Page 108 - CA Final PARAM Digital Book.

P. 108

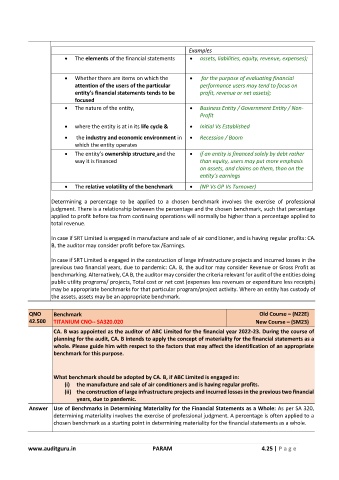

Examples

• The elements of the financial statements • assets, liabilities, equity, revenue, expenses);

• Whether there are items on which the • for the purpose of evaluating financial

attention of the users of the particular performance users may tend to focus on

entity’s financial statements tends to be profit, revenue or net assets);

focused

• The nature of the entity, • Business Entity / Government Entity / Non-

Profit

• where the entity is at in its life cycle & • Initial Vs Established

• the industry and economic environment in • Recession / Boom

which the entity operates

• The entity’s ownership structure and the • if an entity is financed solely by debt rather

way it is financed than equity, users may put more emphasis

on assets, and claims on them, than on the

entity’s earnings

• The relative volatility of the benchmark • (NP Vs GP Vs Turnover)

Determining a percentage to be applied to a chosen benchmark involves the exercise of professional

judgment. There is a relationship between the percentage and the chosen benchmark, such that percentage

applied to profit before tax from continuing operations will normally be higher than a percentage applied to

total revenue.

In case if SRT Limited is engaged in manufacture and sale of air conditioner, and is having regular profits: CA.

B, the auditor may consider profit before tax /Earnings.

In case if SRT Limited is engaged in the construction of large infrastructure projects and incurred losses in the

previous two financial years, due to pandemic: CA. B, the auditor may consider Revenue or Gross Profit as

benchmarking. Alternatively, CA B, the auditor may consider the criteria relevant for audit of the entities doing

public utility programs/ projects, Total cost or net cost (expenses less revenues or expenditure less receipts)

may be appropriate benchmarks for that particular program/project activity. Where an entity has custody of

the assets, assets may be an appropriate benchmark.

QNO Benchmark Old Course – (N22E)

42.500 TITANIUM CNO-- SA320.020 New Course – (SM23)

CA. B was appointed as the auditor of ABC Limited for the financial year 2022-23. During the course of

planning for the audit, CA. B intends to apply the concept of materiality for the financial statements as a

whole. Please guide him with respect to the factors that may affect the identification of an appropriate

benchmark for this purpose.

What benchmark should be adopted by CA. B, if ABC Limited is engaged in:

(i) the manufacture and sale of air conditioners and is having regular profits.

(ii) the construction of large infrastructure projects and incurred losses in the previous two financial

years, due to pandemic.

Answer Use of Benchmarks in Determining Materiality for the Financial Statements as a Whole: As per SA 320,

determining materiality involves the exercise of professional judgment. A percentage is often applied to a

chosen benchmark as a starting point in determining materiality for the financial statements as a whole.

www.auditguru.in PARAM 4.25 | P a g e