Page 154 - CA Final PARAM Digital Book.

P. 154

o Mitigating factors are one which reduces material uncertainty, so sometimes mitigating factors

may nullify material uncertainty.

o There can be circumstances where material uncertainty exists but still chances / probability of

going concern in next 12 months are more and going concern is valid.

QNO Drafting Opinion (Material Uncertainty & No Disclosure in FST) Old Course -- (M22M, M23M)

94.500 TITANIUM CNO--Unique

In the financial year 2020-21, Shreyansh Ltd. faced an extraordinary event (earthquake), which destroyed a

lot of business activity of the company. These circumstances indicate material uncertainty on the company’s

ability to continue as going concern. Due to such event, it may not be possible for the company to realize

its assets or pay off the liabilities during the regular course of its business. The financial statement

and notes to the financial statements of the company do not disclose this fact. What kind of opinion should

the statutory auditor of Shreyansh Ltd. issue in such circumstances and why? Also, draft the

opinion and basis for opinion para for the same.

Answer In the present case, there exists a material uncertainty that cast a significant doubt on the company’s ability

to continue as going concern and the same is not disclosed in the financial statements of Shreyansh Ltd.

As such, the financial statements of Shreyansh Ltd. for the FY 2020-21 are materially misstated and the effect

of the misstatement is so material and pervasive on the financial statements that giving only a qualified

opinion will be insufficient and therefore the statutory auditor of Shreyansh Ltd . should issue an adverse

opinion.

The relevant extract of the Adverse Opinion Paragraph and Basis for Adverse Opinion paragraph is as under:

Adverse Opinion

In our opinion, because of the omission of the information mentioned in the Basis for Adverse Opinion

section of our report, the accompanying financial statements do not present fairly, the financial position of

Shreyansh Ltd. as at March 31, 2021, and of its financial performance and its cash flows for the year then

ended in accordance with the Accounting Standards issued by the Institute of Chartered Accountants of

India.

Basis for Adverse Opinion

Shreyansh Ltd. has faced an extraordinary event (earthquake), which destroyed a lot of business activity of

the company. Due to such event, it may not be possible for the company to realize its assets or pay off the

liabilities during the regular course of its business. This situation indicates that a material uncertainty

exists that may cast significant doubt on the Company’s ability to continue as a going concern. The

financial statement and notes to the financial statements of the company do not disclose this fact.

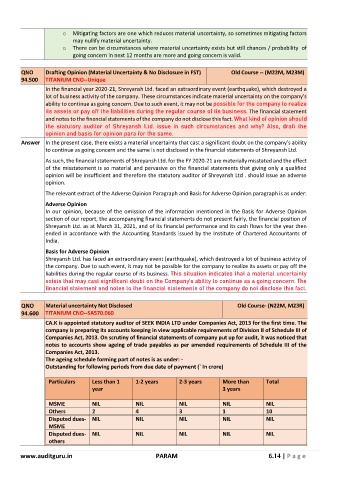

QNO Material uncertainty Not Disclosed Old Course- (N22M, M23R)

94.600 TITANIUM CNO--SA570.060

CA.K is appointed statutory auditor of SEEK INDIA LTD under Companies Act, 2013 for the first time. The

company is preparing its accounts keeping in view applicable requirements of Division II of Schedule III of

Companies Act, 2013. On scrutiny of financial statements of company put up for audit, it was noticed that

notes to accounts show ageing of trade payables as per amended requirements of Schedule III of the

Companies Act, 2013.

The ageing schedule forming part of notes is as under: -

Outstanding for following periods from due date of payment (` In crore)

Particulars Less than 1 1-2 years 2-3 years More than Total

year 3 years

MSME NIL NIL NIL NIL NIL

Others 2 4 3 1 10

Disputed dues- NIL NIL NIL NIL NIL

MSME

Disputed dues- NIL NIL NIL NIL NIL

others

www.auditguru.in PARAM 6.14 | P a g e