Page 182 - CA Final PARAM Digital Book.

P. 182

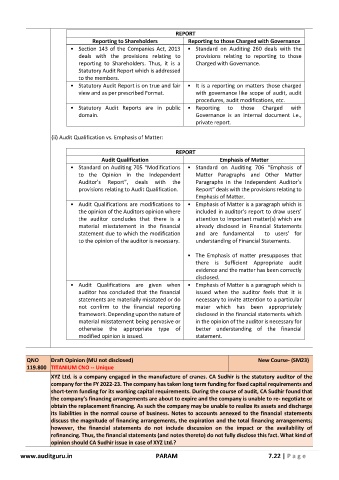

REPORT

Reporting to Shareholders Reporting to those Charged with Governance

• Section 143 of the Companies Act, 2013 • Standard on Auditing 260 deals with the

deals with the provisions relating to provisions relating to reporting to those

reporting to Shareholders. Thus, it is a Charged with Governance.

Statutory Audit Report which is addressed

to the members.

• Statutory Audit Report is on true and fair • It is a reporting on matters those charged

view and as per prescribed Format. with governance like scope of audit, audit

procedures, audit modifications, etc.

• Statutory Audit Reports are in public • Reporting to those Charged with

domain. Governance is an internal document i.e.,

private report.

(ii) Audit Qualification vs. Emphasis of Matter:

REPORT

Audit Qualification Emphasis of Matter

• Standard on Auditing 705 “Modifications • Standard on Auditing 706 “Emphasis of

to the Opinion in the Independent Matter Paragraphs and Other Matter

Auditor’s Report”, deals with the Paragraphs in the Independent Auditor’s

provisions relating to Audit Qualification. Report” deals with the provisions relating to

Emphasis of Matter.

• Audit Qualifications are modifications to • Emphasis of Matter is a paragraph which is

the opinion of the Auditors opinion where included in auditor’s report to draw users’

the auditor concludes that there is a attention to important matter(s) which are

material misstatement in the financial already disclosed in Financial Statements

statement due to which the modification and are fundamental to users’ for

to the opinion of the auditor is necessary. understanding of Financial Statements.

• The Emphasis of matter presupposes that

there is Sufficient Appropriate audit

evidence and the matter has been correctly

disclosed.

• Audit Qualifications are given when • Emphasis of Matter is a paragraph which is

auditor has concluded that the financial issued when the auditor feels that it is

statements are materially misstated or do necessary to invite attention to a particular

not confirm to the financial reporting mater which has been appropriately

framework. Depending upon the nature of disclosed in the financial statements which

material misstatement being pervasive or in the opinion of the auditor is necessary for

otherwise the appropriate type of better understanding of the financial

modified opinion is issued. statement.

QNO Draft Opinion (MU not disclosed) New Course- (SM23)

119.800 TITANIUM CNO -- Unique

XYZ Ltd. is a company engaged in the manufacture of cranes. CA Sudhir is the statutory auditor of the

company for the FY 2022-23. The company has taken long term funding for fixed capital requirements and

short-term funding for its working capital requirements. During the course of audit, CA Sudhir found that

the company’s financing arrangements are about to expire and the company is unable to re- negotiate or

obtain the replacement financing. As such the company may be unable to realize its assets and discharge

its liabilities in the normal course of business. Notes to accounts annexed to the financial statements

discuss the magnitude of financing arrangements, the expiration and the total financing arrangements;

however, the financial statements do not include discussion on the impact or the availability of

refinancing. Thus, the financial statements (and notes thereto) do not fully disclose this fact. What kind of

opinion should CA Sudhir issue in case of XYZ Ltd.?

www.auditguru.in PARAM 7.22 | P a g e