Page 184 - CA Final PARAM Digital Book.

P. 184

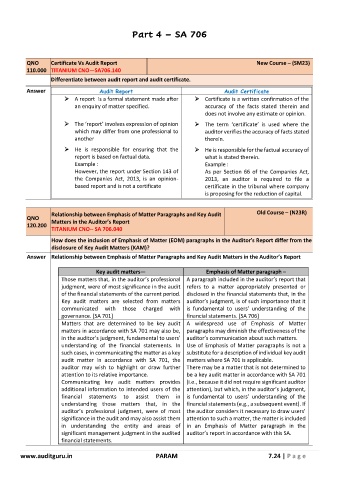

Part 4 – SA 706

QNO Certificate Vs Audit Report New Course – (SM23)

110.000 TITANIUM CNO—SA706.140

Differentiate between audit report and audit certificate.

Answer Audit Report Audit Certificate

➢ A report is a formal statement made after ➢ Certificate is a written confirmation of the

an enquiry of matter specified. accuracy of the facts stated therein and

does not involve any estimate or opinion.

➢ The ‘report’ involves expression of opinion ➢ The term ‘certificate’ is used where the

which may differ from one professional to auditor verifies the accuracy of facts stated

another therein.

➢ He is responsible for ensuring that the ➢ He is responsible for the factual accuracy of

report is based on factual data. what is stated therein.

Example : Example :

However, the report under Section 143 of As per Section 66 of the Companies Act,

the Companies Act, 2013, is an opinion- 2013, an auditor is required to file a

based report and is not a certificate certificate in the tribunal where company

is proposing for the reduction of capital.

Relationship between Emphasis of Matter Paragraphs and Key Audit Old Course – (N23R)

QNO Matters in the Auditor’s Report

120.200

TITANIUM CNO-- SA 706.040

How does the inclusion of Emphasis of Matter (EOM) paragraphs in the Auditor's Report differ from the

disclosure of Key Audit Matters (KAM)?

Answer Relationship between Emphasis of Matter Paragraphs and Key Audit Matters in the Auditor’s Report

Key audit matters— Emphasis of Matter paragraph –

Those matters that, in the auditor’s professional A paragraph included in the auditor’s report that

judgment, were of most significance in the audit refers to a matter appropriately presented or

of the financial statements of the current period. disclosed in the financial statements that, in the

Key audit matters are selected from matters auditor’s judgment, is of such importance that it

communicated with those charged with is fundamental to users’ understanding of the

governance. [SA 701] financial statements. [SA 706]

Matters that are determined to be key audit A widespread use of Emphasis of Matter

matters in accordance with SA 701 may also be, paragraphs may diminish the effectiveness of the

in the auditor’s judgment, fundamental to users’ auditor’s communication about such matters.

understanding of the financial statements. In Use of Emphasis of Matter paragraphs is not a

such cases, in communicating the matter as a key substitute for a description of individual key audit

audit matter in accordance with SA 701, the matters where SA 701 is applicable.

auditor may wish to highlight or draw further There may be a matter that is not determined to

attention to its relative importance. be a key audit matter in accordance with SA 701

Communicating key audit matters provides (i.e., because it did not require significant auditor

additional information to intended users of the attention), but which, in the auditor’s judgment,

financial statements to assist them in is fundamental to users’ understanding of the

understanding those matters that, in the financial statements (e.g., a subsequent event). If

auditor’s professional judgment, were of most the auditor considers it necessary to draw users’

significance in the audit and may also assist them attention to such a matter, the matter is included

in understanding the entity and areas of in an Emphasis of Matter paragraph in the

significant management judgment in the audited auditor’s report in accordance with this SA.

financial statements.

www.auditguru.in PARAM 7.24 | P a g e