Page 15 - Chapter 9 Registration

P. 15

With the help of the above-mentioned information, answer the following questions giving reasons:-

1) Determine whether Mahadev Enterprises is liable to be registered under GST law and what is

the threshold limit of taking registration in this case assuming that it is not required to pay any

tax on inward supplies under reverse charge.

2) Explain with reasons whether your answer in (1) will change in the following independent

cases:-

a) If Mahadev Enterprises is dealing in taxable supply of goods only from Himachal Pradesh;

b) If Mahadev Enterprises is dealing in taxable supply of goods and services only from Himachal

Pradesh;

c) If Mahadev Enterprises is dealing in taxable supply of goods only from Himachal Pradesh and

has also effected inter - State supplies of taxable goods (other than notified handicraft goods &

notified hand-made goods) amounting to ₹ 4,00,000.

[CA Final RTP Nov 19] [Study Mat]

Answer:-

Legal Provision:-

Ü As per section 22 of CGST Act read with Notification No. 10/2019, a supplier is liable to be registered in the

State/ Union territory from where he makes a taxable supply of goods and/or services, if his aggregate

turnover in a financial year exceeds the threshold limit.

Ü The threshold limit for a person making exclusive supply of services or supply of both goods and

services is as under:-

Ø ₹ 10 lakh for the Special Category States of Mizoram, Tripura, Manipur and Nagaland.

Ø ₹ 20 lakh for the rest of India.

Ü The threshold limit for a person making exclusive intra-state supplies of goods:-

Ø ₹ 10 lakh for the Special Category States of Mizoram, Tripura, Manipur and Nagaland.

Ø ₹ 20 lakh for the States of Arunachal Pradesh, Meghalaya, Puducherry, Sikkim, Telangana and

Uttarakhand.

Ø ₹ 40 lakh for rest of India.

Ü As per section 2(6) of CGST Act, 2017, “aggregate turnover” means the aggregate value of all taxable

supplies, exempt supplies (wholly exempt, nil rated & Non-taxable), exports & inter-State supplies of

persons having same Permanent Account Number, to be computed on all India basis.

Discussion:-

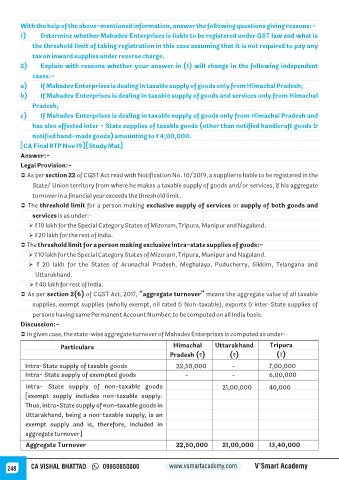

Ü In given case, the state-wise aggregate turnover of Mahadev Enterprises is computed as under:-

Particulars Himachal Uttarakhand Tripura

Pradesh (₹) (₹) (₹)

Intra-State supply of taxable goods 22,50,000 - 7,00,000

Intra- State supply of exempted goods - - 6,00,000

Intra- State supply of non-taxable goods 21,00,000 40,000

[exempt supply includes non-taxable supply.

Thus, intra-State supply of non-taxable goods in

Uttarakhand, being a non-taxable supply, is an

exempt supply and is, therefore, included in

aggregate turnover]

Aggregate Turnover 22,50,000 21,00,000 13,40,000

248 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy