Page 13 - Chapter 9 Registration

P. 13

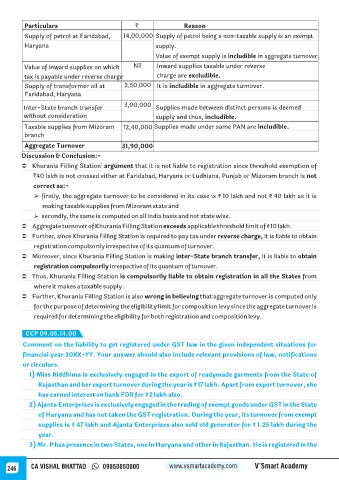

Particulars ` Reason

Supply of petrol at Faridabad, 14,00,000 Supply of petrol being a non-taxable supply is an exempt

Haryana supply.

Value of exempt supply is includible in aggregate turnover.

Value of inward supplies on which Nil Inward supplies taxable under reverse

tax is payable under reverse charge charge are excludible.

Supply of transformer oil at 2,50,000 It is includible in aggregate turnover.

Faridabad, Haryana

3,00,000

Inter-State branch transfer Supplies made between distinct persons is deemed

without consideration supply and thus, includible.

Taxable supplies from Mizoram 12,40,000 Supplies made under same PAN are includible.

branch

Aggregate Turnover 31,90,000

Discussion & Conclusion:-

Ü Khurania Filling Station' argument that it is not liable to registration since threshold exemption of

`40 lakh is not crossed either at Faridabad, Haryana or Ludhiana, Punjab or Mizoram branch is not

correct as:-

Ø firstly, the aggregate turnover to be considered in its case is ₹ 10 lakh and not ₹ 40 lakh as it is

making taxable supplies from Mizoram state and

Ø secondly, the same is computed on all India basis and not state wise.

Ü Aggregate turnover of Khurania Filling Station exceeds applicable threshold limit of ₹ 10 lakh.

Ü Further, since Khurania Filling Station is required to pay tax under reverse charge, it is liable to obtain

registration compulsorily irrespective of its quantum of turnover.

Ü Moreover, since Khurania Filling Station is making inter-State branch transfer, it is liable to obtain

registration compulsorily irrespective of its quantum of turnover.

Ü Thus, Khurania Filling Station is compulsorily liable to obtain registration in all the States from

where it makes a taxable supply.

Ü Further, Khurania Filling Station is also wrong in believing that aggregate turnover is computed only

for the purpose of determining the eligibility limit for composition levy since the aggregate turnover is

required for determining the eligibility for both registration and composition levy.

CCP 09.05.14.00

Comment on the liability to get registered under GST law in the given independent situations for

financial year 20XX-YY. Your answer should also include relevant provisions of law, notifications

or circulars.

1) Miss Riddhima is exclusively engaged in the export of readymade garments from the State of

Rajasthan and her export turnover during the year is ₹ 17 lakh. Apart from export turnover, she

has earned interest on bank FDR for ₹ 2 lakh also.

2) Ajanta Enterprises is exclusively engaged in the trading of exempt goods under GST in the State

of Haryana and has not taken the GST registration. During the year, its turnover from exempt

supplies is ₹ 47 lakh and Ajanta Enterprises also sold old generator for ₹ 1.25 lakh during the

year.

3) Mr. P has presence in two States, one in Haryana and other in Rajasthan. He is registered in the

246 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy