Page 14 - Chapter 9 Registration

P. 14

State of Rajasthan even without crossing the threshold limit. His turnover during the year in

Rajasthan is ₹ 32 lakh and in Haryana is ₹ 5 lakh. Is he mandatorily required to get registered in

the State of Haryana also?

4) Mr. John is engaged in the business of buying and selling of shares on his own account from the

secondary market and his income from this activity is assessed as business income under the

Income-tax Act 1961. During the year his total sales turnover from shares was ₹ 90 lakh.

[CA Final Dec 21 Exam]

Answer:-

1 Ü Export of goods is treated as inter-State supply.

Ü Miss Riddhima is liable to obtain registration compulsorily irrespective of the quantum of her

aggregate turnover since she is engaged in making inter-State supply (exports) of goods.

Ü It is assumed that the exporter of goods – Miss Riddhima – has availed the export benefits

available under GST.

2 Ü Any person engaged exclusively in making exempt supplies is not liable to registration.

Ü However, Ajanta Enterprises is liable to get registered as it has also made a taxable supply along

with exempt supplies during the year and its aggregate turnover (₹ 48.25 lakh) exceeds the

threshold limit for registration (Rs. 40 lakhs).

3 Ü Since registration in GST is PAN based, once a supplier is liable to register, he has to obtain

registration in each of the States/Union Territories in which he operates under the same PAN.

Ü Thus, Mr. P is liable to get registered in Haryana also, provided he is not engaged exclusively in

making exempt supplies from Haryana.

Ü However, a person who is voluntarily registered in one State needs to obtain registration in other

States from where he makes a taxable supply only if his aggregate turnover exceeds applicable

threshold limit for registration. In that case, Mr. P is not liable to obtain registration from

Haryana since the aggregate turnover does not exceed the threshold limit for registration

4 Ü A supplier is liable to obtain registration in a State/Union Territory from where he makes taxable

supply of goods and/or services.

Ü Shares are excluded from the definition of goods as well as services & hence, buying and selling of

shares is not a supply of goods and/or services under GST law.

Ü Thus, Mr. John is not liable to obtain registration since he is not engaged in making a taxable

supply of goods and/or services.

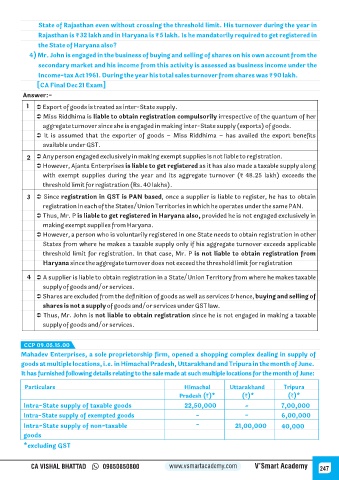

CCP 09.05.15.00

Mahadev Enterprises, a sole proprietorship firm, opened a shopping complex dealing in supply of

goods at multiple locations, i.e. in Himachal Pradesh, Uttarakhand and Tripura in the month of June.

It has furnished following details relating to the sale made at such multiple locations for the month of June:

Particulars Himachal Uttarakhand Tripura

Pradesh (`)* (`)* (`)*

Intra-State supply of taxable goods 22,50,000 - 7,00,000

Intra-State supply of exempted goods - - 6,00,000

Intra-State supply of non-taxable - 21,00,000 40,000

goods

*excluding GST

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 247