Page 41 - Chap24Computation of GST

P. 41

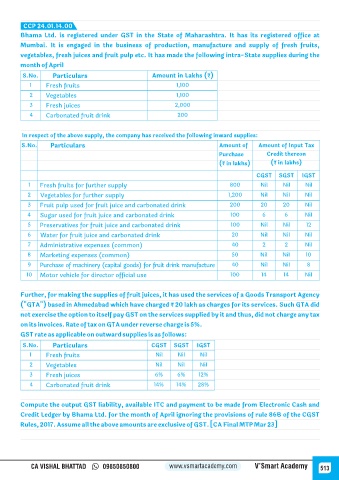

CCP 24.01.14.00

Bhama Ltd. is registered under GST in the State of Maharashtra. It has its registered office at

Mumbai. It is engaged in the business of production, manufacture and supply of fresh fruits,

vegetables, fresh juices and fruit pulp etc. It has made the following intra-State supplies during the

month of April

S.No. Particulars Amount in Lakhs (₹)

1 Fresh fruits 1,100

2 Vegetables 1,100

3 Fresh juices 2,000

4 Carbonated fruit drink 200

In respect of the above supply, the company has received the following inward supplies:

S.No. Particulars Amount of Amount of Input Tax

Purchase Credit thereon

(₹ in lakhs) (₹ in lakhs)

CGST SGST IGST

1 Fresh fruits for further supply 800 Nil Nil Nil

2 Vegetables for further supply 1,200 Nil Nil Nil

3 Fruit pulp used for fruit juice and carbonated drink 200 20 20 Nil

4 Sugar used for fruit juice and carbonated drink 100 6 6 Nil

5 Preservatives for fruit juice and carbonated drink 100 Nil Nil 12

6 Water for fruit juice and carbonated drink 20 Nil Nil Nil

7 Administrative expenses (common) 40 2 2 Nil

8 Marketing expenses (common) 50 Nil Nil 10

9 Purchase of machinery (capital goods) for fruit drink manufacture 40 Nil Nil 8

10 Motor vehicle for director official use 100 14 14 Nil

Further, for making the supplies of fruit juices, it has used the services of a Goods Transport Agency

("GTA") based in Ahmedabad which have charged ₹ 20 lakh as charges for its services. Such GTA did

not exercise the option to itself pay GST on the services supplied by it and thus, did not charge any tax

on its invoices. Rate of tax on GTA under reverse charge is 5%.

GST rate as applicable on outward supplies is as follows:

S.No. Particulars CGST SGST IGST

1 Fresh fruits Nil Nil Nil

2 Vegetables Nil Nil Nil

3 Fresh juices 6% 6% 12%

4 Carbonated fruit drink 14% 14% 28%

Compute the output GST liability, available ITC and payment to be made from Electronic Cash and

Credit Ledger by Bhama Ltd. for the month of April ignoring the provisions of rule 86B of the CGST

Rules, 2017. Assume all the above amounts are exclusive of GST. [CA Final MTP Mar 23]

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 513