Page 36 - Chap24Computation of GST

P. 36

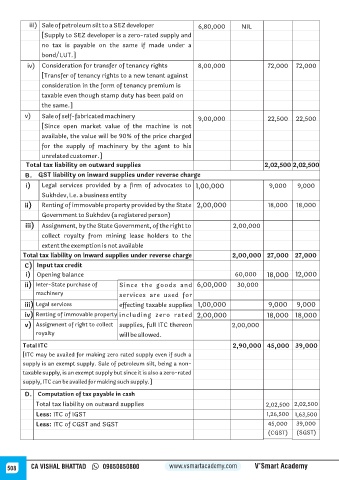

iii) Sale of petroleum silt to a SEZ developer 6,80,000 NIL

[Supply to SEZ developer is a zero-rated supply and

no tax is payable on the same if made under a

bond/LUT.]

iv) Consideration for transfer of tenancy rights 8,00,000 72,000 72,000

[Transfer of tenancy rights to a new tenant against

consideration in the form of tenancy premium is

taxable even though stamp duty has been paid on

the same.]

v) Sale of self-fabricated machinery

9,00,000 22,500 22,500

[Since open market value of the machine is not

available, the value will be 90% of the price charged

for the supply of machinery by the agent to his

unrelated customer.]

Total tax liability on outward supplies 2,02,500 2,02,500

B. GST liability on inward supplies under reverse charge

i) Legal services provided by a firm of advocates to 1,00,000 9,000 9,000

Sukhdev, i.e. a business entity

ii) Renting of immovable property provided by the State 2,00,000 18,000 18,000

Government to Sukhdev (a registered person)

iii) Assignment, by the State Government, of the right to 2,00,000

collect royalty from mining lease holders to the

extent the exemption is not available

Total tax liability on inward supplies under reverse charge 2,00,000 27,000 27,000

C) Input tax credit

i) Opening balance 60,000 18,000 12,000

ii) Inter-State purchase of Since the goods and 6,00,000 30,000

machinery services are used for

iii) Legal services effecting taxable supplies 1,00,000 9,000 9,000

iv) Renting of immovable property including zero rated 2,00,000 18,000 18,000

v) Assignment of right to collect supplies, full ITC thereon 2,00,000

royalty will be allowed.

Total ITC 2,90,000 45,000 39,000

[ITC may be availed for making zero rated supply even if such a

supply is an exempt supply. Sale of petroleum silt, being a non-

taxable supply, is an exempt supply but since it is also a zero-rated

supply, ITC can be availed for making such supply.]

D. Computation of tax payable in cash

Total tax liability on outward supplies 2,02,500 2,02,500

Less: ITC of IGST 1,26,500 1,63,500

Less: ITC of CGST and SGST 45,000 39,000

(CGST) (SGST)

508 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy