Page 39 - Chap24Computation of GST

P. 39

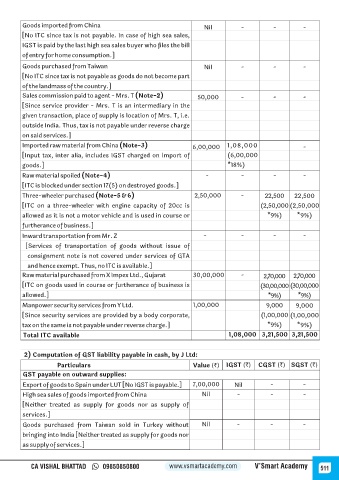

Goods imported from China Nil - - -

[No ITC since tax is not payable. In case of high sea sales,

IGST is paid by the last high sea sales buyer who files the bill

of entry for home consumption.]

Goods purchased from Taiwan Nil - - -

[No ITC since tax is not payable as goods do not become part

of the landmass of the country.]

Sales commission paid to agent - Mrs. T (Note-2) 50,000 - - -

[Since service provider - Mrs. T is an intermediary in the

given transaction, place of supply is location of Mrs. T, i.e.

outside India. Thus, tax is not payable under reverse charge

on said services.]

Imported raw material from China (Note-3) 6,00,000 1,08,000 -

-

[Input tax, inter alia, includes IGST charged on import of (6,00,000

goods.] *18%)

Raw material spoiled (Note-4) - - - -

[ITC is blocked under section 17(5) on destroyed goods.]

Three-wheeler purchased (Note-5 & 6) 2,50,000 - 22,500 22,500

[ITC on a three-wheeler with engine capacity of 20cc is (2,50,000 (2,50,000

allowed as it is not a motor vehicle and is used in course or *9%) *9%)

furtherance of business.]

Inward transportation from Mr. Z - - - -

[Services of transportation of goods without issue of

consignment note is not covered under services of GTA

and hence exempt. Thus, no ITC is available.]

Raw material purchased from X Impex Ltd., Gujarat 30,00,000 - 2,70,000 2,70,000

[ITC on goods used in course or furtherance of business is (30,00,000 (30,00,000

allowed.] *9%) *9%)

Manpower security services from Y Ltd. 1,00,000 9,000 9,000

[Since security services are provided by a body corporate, (1,00,000 (1,00,000

tax on the same is not payable under reverse charge.] *9%) *9%)

Total ITC available 1,08,000 3,21,500 3,21,500

2) Computation of GST liability payable in cash, by J Ltd:

Particulars Value (`) IGST (`) CGST (`) SGST (`)

GST payable on outward supplies:

Export of goods to Spain under LUT [No IGST is payable.] 7,00,000 Nil - -

High sea sales of goods imported from China Nil - - -

[Neither treated as supply for goods nor as supply of

services.]

Goods purchased from Taiwan sold in Turkey without Nil - - -

bringing into India [Neither treated as supply for goods nor

as supply of services.]

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 511