Page 37 - Chap24Computation of GST

P. 37

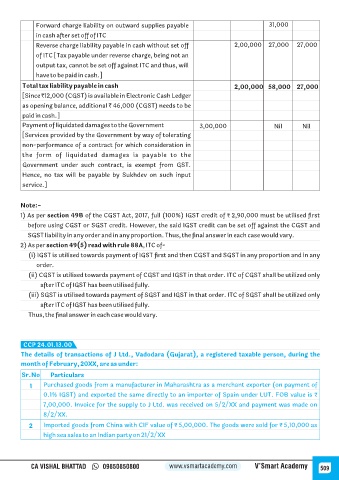

Forward charge liability on outward supplies payable 31,000

in cash after set off of ITC

Reverse charge liability payable in cash without set off 2,00,000 27,000 27,000

of ITC [Tax payable under reverse charge, being not an

output tax, cannot be set off against ITC and thus, will

have to be paid in cash.]

Total tax liability payable in cash 2,00,000 58,000 27,000

[Since `12,000 (CGST) is available in Electronic Cash Ledger

as opening balance, additional ` 46,000 (CGST) needs to be

paid in cash.]

Payment of liquidated damages to the Government 3,00,000 Nil Nil

[Services provided by the Government by way of tolerating

non-performance of a contract for which consideration in

the form of liquidated damages is payable to the

Government under such contract, is exempt from GST.

Hence, no tax will be payable by Sukhdev on such input

service.]

Note:-

1) As per section 49B of the CGST Act, 2017, full (100%) IGST credit of ₹ 2,90,000 must be utilised first

before using CGST or SGST credit. However, the said IGST credit can be set off against the CGST and

SGST liability in any order and in any proportion. Thus, the final answer in each case would vary.

2) As per section 49(5) read with rule 88A, ITC of-

(i) IGST is utilised towards payment of IGST first and then CGST and SGST in any proportion and in any

order.

(ii) CGST is utilised towards payment of CGST and IGST in that order. ITC of CGST shall be utilized only

after ITC of IGST has been utilised fully.

(iii) SGST is utilised towards payment of SGST and IGST in that order. ITC of SGST shall be utilized only

after ITC of IGST has been utilised fully.

Thus, the final answer in each case would vary.

CCP 24.01.13.00

The details of transactions of J Ltd., Vadodara (Gujarat), a registered taxable person, during the

month of February, 20XX, are as under:

Sr.No Particulars

1 Purchased goods from a manufacturer in Maharashtra as a merchant exporter (on payment of

0.1% IGST) and exported the same directly to an importer of Spain under LUT. FOB value is ₹

7,00,000. Invoice for the supply to J Ltd. was received on 5/2/XX and payment was made on

8/2/XX.

2 Imported goods from China with CIF value of ₹ 5,00,000. The goods were sold for ₹ 5,10,000 as

high sea sales to an Indian party on 21/2/XX

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 509