Page 38 - Chap24Computation of GST

P. 38

Purchased goods from a party in Taiwan. Sold the goods to a party in Turkey without bringing the

3

goods to India. Purchase value was ₹ 5,00,000 and the sale price was ₹ 7,00,000. J Ltd paid sales

commission of ₹ 50,000 to Mrs. T, their agent in connection with this transaction. The

transaction was completed in the third week of February. (The figures in rupees have been given

after conversion though transaction was in convertible foreign currency).

J Ltd. has agreed to provide technical services to Mr. K of Ahmedabad who is an unregistered

4

person in connection with the manufacturing operations to be undertaken by him for a

consideration of ₹ 5,00,000 and has received an advance of ₹ 1,00,000 for the same on 2/2/XX.

5 It has imported raw materials from China. CIF value of the goods for the purpose of Customs

included ₹ 1,00,000 as ocean freight paid by J Ltd. The value for the purpose of levy of IGST worked

out by Customs was ₹ 6,00,000. Clearance of the goods took place on 4/2/XX

6 Locally purchased taxable raw material stored in the factory got spoiled due to rainwater in the

factory and became unusable. J Ltd. claimed and received on insurance amount of ₹ 60,000 for

the same. Value of the raw material at the time of receipt was ₹ 70,000. Raw material was

purchased from a party in Gujarat on 3/2/XX and payment was made on 7/2/XX

7 Company purchased a three-wheeler having capacity of 2 persons including driver (engine

capacity 20CC) at a cost of ₹ 2,50,000 which is being used for transportation of staff of company

from residence to factory and back. The vehicle was received on 5/2/XX and payment was made on

the same date

8 It has paid inward transportation expense of ₹ 30,000 to Mr. Z, a tempo owner who has not issued any

consignment notes. He has issued a consolidated bill only on 3/2/XX and payment was made on 4/2/XX.

9 It has supplied goods of value of ₹ 50,00,000 to V Ltd. Padra, Gujarat (includes ₹ 10,00,000

supplied to SEZ unit of V Ltd).

10 It has purchased goods from X Impex Ltd. Kadi, Gujarat for use as raw materials in its factory. The

value of the goods ₹ 30,00,000. Invoice is dated 2/2/20XX.

11 It has availed supply of manpower security services from Y Ltd. Vadodara, Gujarat, a registered

taxable person. The amount paid is ₹ 1,00,000. The invoice was received on 1/2/20XX and

payment was made on the same day.

Assume the CGST and SGST rates to be 9% each and IGST rate to be 18% except the supply received as

a merchant exporter. Ignore compensation cess. J Ltd. had an opening balance of ITC of CGST of ₹

20,000 and SGST of ₹ 20,000 as on 1/2/20XX. In respect of all the inward supplies, suppliers have

uploaded their invoices in respective Form GSTR-1 and the supplies are reflected in GSTR-2A/2B. All

the figures given above are exclusive of GST, wherever applicable.

Work out the admissible ITC and GST liability [CGST, SGST or IGST, as the case may be] payable in

cash, by J Ltd, Vadodara (Gujarat), for February, 20XX.

Ensure that all the items in the table are covered in your answer. Provide supporting explanatory

notes for your conclusion wherever required. [CA Final Nov 22 Exam]

Answer:

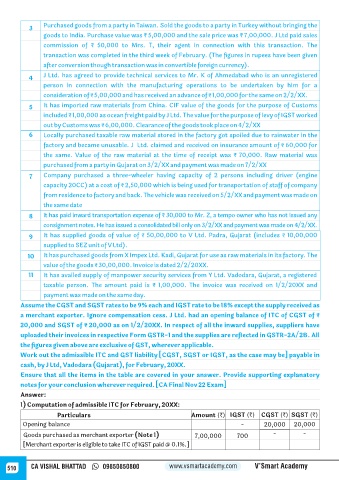

1) Computation of admissible ITC for February, 20XX:

Particulars Amount (`) IGST (`) CGST (`) SGST (`)

Opening balance - 20,000 20,000

Goods purchased as merchant exporter (Note 1) 7,00,000 700 - -

[Merchant exporter is eligible to take ITC of IGST paid @ 0.1%.]

510 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy