Page 20 - Chap7 ITC

P. 20

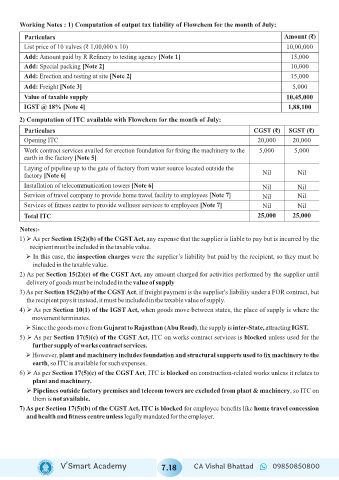

Working Notes : 1) Computation of output tax liability of Flowchem for the month of July:

Particulars Amount (₹)

List price of 10 valves (₹ 1,00,000 x 10) 10,00,000

Add: Amount paid by R Refinery to testing agency [Note 1] 15,000

Add: Special packing [Note 2] 10,000

Add: Erection and testing at site [Note 2] 15,000

Add: Freight [Note 3] 5,000

Value of taxable supply 10,45,000

IGST @ 18% [Note 4] 1,88,100

2) Computation of ITC available with Flowchem for the month of July:

Particulars CGST (₹) SGST (₹)

Opening ITC 20,000 20,000

Work contract services availed for erection foundation for fixing the machinery to the 5,000 5,000

earth in the factory [Note 5]

Laying of pipeline up to the gate of factory from water source located outside the

factory [Note 6] Nil Nil

Installation of telecommunication towers [Note 6] Nil Nil

Services of travel company to provide home travel facility to employees [Note 7] Nil Nil

Services of fitness centre to provide wellness services to employees [Note 7] Nil Nil

Total ITC 25,000 25,000

Notes:-

1) Ø As per Section 15(2)(b) of the CGST Act, any expense that the supplier is liable to pay but is incurred by the

recipient must be included in the taxable value.

Ø In this case, the inspection charges were the supplier’s liability but paid by the recipient, so they must be

included in the taxable value.

2) As per Section 15(2)(c) of the CGST Act, any amount charged for activities performed by the supplier until

delivery of goods must be included in the value of supply

3) As per Section 15(2)(b) of the CGST Act, if freight payment is the supplier's liability under a FOR contract, but

the recipient pays it instead, it must be included in the taxable value of supply.

4) Ø As per Section 10(1) of the IGST Act, when goods move between states, the place of supply is where the

movement terminates.

Ø Since the goods move from Gujarat to Rajasthan (Abu Road), the supply is inter-State, attracting IGST.

5) Ø As per Section 17(5)(c) of the CGST Act, ITC on works contract services is blocked unless used for the

further supply of works contract services.

Ø However, plant and machinery includes foundation and structural supports used to fix machinery to the

earth, so ITC is available for such expenses.

6) Ø As per Section 17(5)(c) of the CGST Act, ITC is blocked on construction-related works unless it relates to

plant and machinery.

Ø Pipelines outside factory premises and telecom towers are excluded from plant & machinery, so ITC on

them is not available.

7) As per Section 17(5)(b) of the CGST Act, ITC is blocked for employee benefits like home travel concession

and health and fitness centre unless legally mandated for the employer.

V’Smart Academy 7.18 CA Vishal Bhattad 09850850800