Page 22 - Chap7 ITC

P. 22

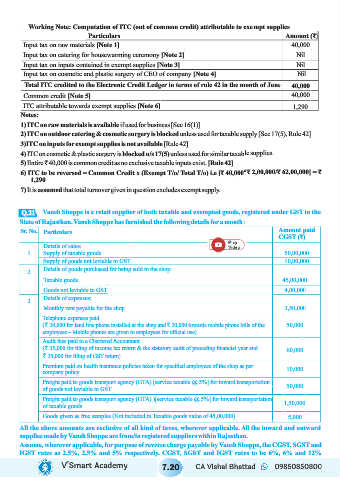

Working Note: Computation of ITC (out of common credit) attributable to exempt supplies

Particulars Amount (₹)

Input tax on raw materials [Note 1] 40,000

Input tax on catering for housewarming ceremony [Note 2] Nil

Input tax on inputs contained in exempt supplies [Note 3] Nil

Input tax on cosmetic and plastic surgery of CEO of company [Note 4] Nil

Total ITC credited to the Electronic Credit Ledger in terms of rule 42 in the month of June 40,000

Common credit [Note 5] 40,000

ITC attributable towards exempt supplies [Note 6] 1,290

Notes:

1) ITC on raw materials is available if used for business [Sec 16(1)]

2) ITC on outdoor catering & cosmetic surgery is blocked unless used for taxable supply [Sec 17(5), Rule 42]

3)ITC on inputs for exempt supplies is not available [Rule 42]

4) ITC on cosmetic & plastic surgery is blocked u/s 17(5) unless used for similar taxable supplies.

5) Entire ₹ 40,000 is common credit as no exclusive taxable inputs exist. [Rule 42]

6) ITC to be reversed = Common Credit x (Exempt T/o/ Total T/o) i.e [₹ 40,000*₹ 2,00,000/₹ 62,00,000] = ₹

1,290

7) It is assumed that total turnover given in question excludes exempt supply.

Q.21 Vansh Shoppe is a retail supplier of both taxable and exempted goods, registered under GST in the

State of Rajasthan. Vansh Shoppe has furnished the following details for a month:

Sr. No. Particulars Amount paid

CGST (₹)

Details of sales:

1. Supply of taxable goods 50,00,000

Supply of goods not leviable to GST 10,00,000

Details of goods purchased for being sold in the shop:

2.

Taxable goods 45,00,000

Goods not leviable to GST 4,00,000

Details of expenses:

3.

Monthly rent payable for the shop 3,50,000

Telephone expenses paid

( 30,000 for land line phone installed at the shop and 20,000 towards mobile phone bills of the ₹ ₹ 50,000

employees – Mobile phones are given to employees for official use)

Audit fees paid to a Chartered Accountant

(₹ 35,000 for filing of income tax return & the statutory audit of preceding financial year and 60,000

₹ 25,000 for filing of GST return)

Premium paid on health insurance policies taken for specified employees of the shop as per 10,000

company policy.

Freight paid to goods transport agency (GTA) [service taxable @ 5%] for inward transportation 50,000

of goods not leviable to GST

Freight paid to goods transport agency (GTA) )[service taxable @ 5%] for inward transportation

1,50,000

of taxable goods

Goods given as free samples (Not included in Taxable goods value of 45,00,000) 5,000

All the above amounts are exclusive of all kind of taxes, wherever applicable. All the inward and outward

supplies made by Vansh Shoppe are from/to registered suppliers within Rajasthan.

Assume, wherever applicable, for purpose of reverse charge payable by Vansh Shoppe, the CGST, SGST and

IGST rates as 2.5%, 2.5% and 5% respectively. CGST, SGST and IGST rates to be 6%, 6% and 12%

V’Smart Academy 7.20 CA Vishal Bhattad 09850850800