Page 23 - Chap7 ITC

P. 23

respectively in all other cases. There is no opening balance in the electronic cash ledger or electronic credit

ledger. Subject to the information given above, assume that all the other conditions necessary for availing

ITC have been fulfilled.

You are required to compute the following:

(1) Input Tax Credit (ITC) credited to Electronic Credit Ledger

(2) Common credit available for apportionment

(3) ITC attributable towards exempt supplies out of common credit

(4) Net GST payable from Electronic Cash Ledger for the month [Study Mat] [CA Final MTP 1 May 25]

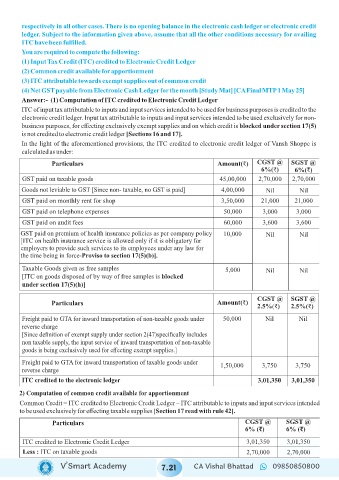

Answer:- (1) Computation of ITC credited to Electronic Credit Ledger

ITC of input tax attributable to inputs and input services intended to be used for business purposes is credited to the

electronic credit ledger. Input tax attributable to inputs and input services intended to be used exclusively for non-

business purposes, for effecting exclusively exempt supplies and on which credit is blocked under section 17(5)

is not credited to electronic credit ledger [Sections 16 and 17].

In the light of the aforementioned provisions, the ITC credited to electronic credit ledger of Vansh Shoppe is

calculated as under:

Particulars Amount(₹) CGST @ SGST @

6%(₹) 6%(₹)

GST paid on taxable goods 45,00,000 2,70,000 2,70,000

Goods not leviable to GST [Since non- taxable, no GST is paid] 4,00,000 Nil Nil

GST paid on monthly rent for shop 3,50,000 21,000 21,000

GST paid on telephone expenses 50,000 3,000 3,000

GST paid on audit fees 60,000 3,600 3,600

GST paid on premium of health insurance policies as per company policy 10,000 Nil Nil

[ITC on health insurance service is allowed only if it is obligatory for

employers to provide such services to its employees under any law for

the time being in force-Proviso to section 17(5)(b)].

Taxable Goods given as free samples 5,000 Nil Nil

[ITC on goods disposed of by way of free samples is blocked

under section 17(5)(h)]

CGST @ SGST @

Particulars Amount(₹)

2.5%(₹) 2.5%(₹)

Freight paid to GTA for inward transportation of non-taxable goods under 50,000 Nil Nil

reverse charge

[Since definition of exempt supply under section 2(47)specifically includes

non taxable supply, the input service of inward transportation of non-taxable

goods is being exclusively used for effecting exempt supplies.]

Freight paid to GTA for inward transportation of taxable goods under

1,50,000 3,750 3,750

reverse charge

ITC credited to the electronic ledger 3,01,350 3,01,350

2) Computation of common credit available for apportionment

Common Credit = ITC credited to Electronic Credit Ledger – ITC attributable to inputs and input services intended

to be used exclusively for effecting taxable supplies [Section 17 read with rule 42].

Particulars CGST @ SGST @

6% (₹) 6% (₹)

ITC credited to Electronic Credit Ledger 3,01,350 3,01,350

Less : ITC on taxable goods 2,70,000 2,70,000

V’Smart Academy 7.21 CA Vishal Bhattad 09850850800