Page 27 - Chap7 ITC

P. 27

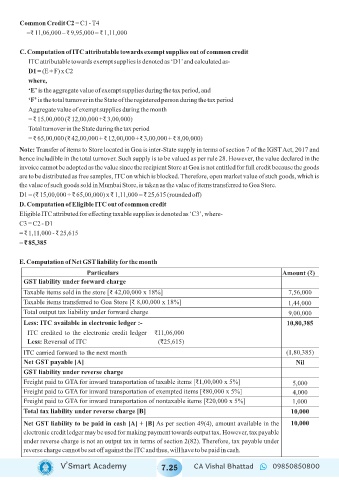

Common Credit C2 = C1 - T4

= 11,06,000 – 9,95,000 = 1,11,000₹ ₹ ₹

C. Computation of ITC attributable towards exempt supplies out of common credit

ITC attributable towards exempt supplies is denoted as ‘D1’ and calculated as-

D1 = (E ÷ F) x C2

where,

‘E’ is the aggregate value of exempt supplies during the tax period, and

‘F’ is the total turnover in the State of the registered person during the tax period

Aggregate value of exempt supplies during the month

= 15,00,000 ( 12,00,000 + 3,00,000)₹ ₹ ₹

Total turnover in the State during the tax period

= 65,00,000 ( 42,00,000 + 12,00,000 + 3,00,000 + 8,00,000)₹ ₹ ₹ ₹ ₹

Note: Transfer of items to Store located in Goa is inter-State supply in terms of section 7 of the IGST Act, 2017 and

hence includible in the total turnover. Such supply is to be valued as per rule 28. However, the value declared in the

invoice cannot be adopted as the value since the recipient Store at Goa is not entitled for full credit because the goods

are to be distributed as free samples, ITC on which is blocked. Therefore, open market value of such goods, which is

the value of such goods sold in Mumbai Store, is taken as the value of items transferred to Goa Store.

D1 = ( 15,00,000 ÷ 65,00,000) x 1,11,000 = 25,615 (rounded off)₹ ₹ ₹ ₹

D. Computation of Eligible ITC out of common credit

Eligible ITC attributed for effecting taxable supplies is denoted as ‘C3’, where-

C3 = C2 - D1

= 1,11,000 - 25,615₹ ₹

= 85,385₹

E. Computation of Net GST liability for the month

Particulars Amount ( )₹

GST liability under forward charge

Taxable items sold in the store [ 42,00,000 x 18%]₹ 7,56,000

Taxable items transferred to Goa Store [ 8,00,000 x 18%]₹ 1,44,000

Total output tax liability under forward charge 9,00,000

Less: ITC available in electronic ledger :- 10,80,385

ITC credited to the electronic credit ledger 11,06,000₹

Less: Reversal of ITC ( 25,615)₹

ITC carried forward to the next month (1,80,385)

Net GST payable [A] Nil

GST liability under reverse charge

Freight paid to GTA for inward transportation of taxable items [ 1,00,000 x 5%]₹ 5,000

Freight paid to GTA for inward transportation of exempted items [ 80,000 x 5%]₹ 4,000

Freight paid to GTA for inward transportation of nontaxable items [ 20,000 x 5%]₹ 1,000

Total tax liability under reverse charge [B] 10,000

Net GST liability to be paid in cash [A] + [B] As per section 49(4), amount available in the 10,000

electronic credit ledger may be used for making payment towards output tax. However, tax payable

under reverse charge is not an output tax in terms of section 2(82). Therefore, tax payable under

reverse charge cannot be set off against the ITC and thus, will have to be paid in cash.

V’Smart Academy 7.25 CA Vishal Bhattad 09850850800